Growth Verses Growths

In my last post, I tried to flesh out how the gold standard backing money worked, focusing on the fact that a dollar's worth of gold does not back a dollar's worth of paper currency. That myth simply needs to be put to rest. Retiring myths is difficult, however, unless everyone understand how the gold standard really works.

In this post, I would like to put forth my conjecture about how the current system of loans works fairly well as a back to our money supply, but how several of the largest banks have perverted that system in pursuit of ever greater returns on their money. I ended that last post by demonstrating how a dollar's worth of gold under the gold standard backs a greater amount of paper money. This illustration shows a 6:1 reserve:

The above illustration shows what money was like under the gold standard, a system we no longer follow. Since the latest economic crisis was largely blamed on the housing market, let's replace that coin with a more appropriate symbol:

Let's say you would like to buy this house. You walk into a bank and ask for a home loan. The loan officer reviews (or should review) your ability to pay the bank a regular payment over the next 30 years or so. If you pass this inspection, the bank creates a large pile of money that previous to the loan creation simply didn't exist. With this money you buy the house. In return for the new money, the bank gets an asset; either the loan amount (newly created principal plus interest) or, should you fail to pay as agreed, the foreclosed house. Even if you sell the house before the mortgage is payed in full, the bank gets the principal amount returned.

So, what backs this money? There's no gold, no silver. Critics call this system Fiat money, "fiat" Latin for "let it be done." From the Wiki:

While specie-backed representative money entails the legal requirement that the bank of issue redeem it in fixed weights of specie, fiat money's value is unrelated to the value of any physical quantity. Even a coin containing valuable metal may be considered fiat currency if its face value is higher than its market value as metal.

I italicized that above section because I fundamentally disagree with the Wiki author's declaration. The newly-created money from our speculative scenario is related to a "physical quantity" -- the house.

This might seem endlessly recursive, but only because, well, it is. The value of today's money is pegged to the value of the items held as collateral for the loans that generated the money. In the traditional version of our economic and monetary system, this works pretty well. After all, the homeowner that buys my gray house with the red door does indeed have to pay the mortgage; but he or she avoids the rent that furnished the previous shelter. Owner-occupied homes tend to be maintained better than rentals. (That last sentence is admittedly a bit speculative and based only on my experience living in both environments, predominantly rental neighborhoods and predominantly owner-occupied. A good friend used to have a saying: "Rental; based on the Latin root, to thrash." I would like to see quality-of-life statistics comparing the two types of neighborhoods to either confirm or deny this assertion; but until proven wrong I'm going to stick by this statement.) Thus, I'm going out on a limb and state that densities of predominantly owner-occupied houses raise the value of all the homes in the neighborhood by raising the desirability of the entire neighborhood; furthermore that creating money through loans to create owner-occupied neighborhoods creates real value that supports both the money created and the items procured by that creation.

Let's also remember that loans need not buy only houses. They can also buy equipment for all manner of production, from home construction to factories to software to farms.

I'll say it again: the value of the dollars in our economy is literally in the items bought with the loans that created those dollars. The more closely connected these productive items are to the money produced for their purchase -- the more directly the money that bought these items that "work" to "drive" the myriad activities that produce our food, our shelter, our transportation, our production and our creation -- the stronger both our economy and our monetary system is.

And here we have the problem. What if these items are increasingly distant from the money they support, the money they back, the money created by the loans that bought them? Worse, what if the money created by loans are created for items that have no intrinsic or lasting value? The last thirty years have brought mechanisms to our monetary system that have like a cancer metastasized our money supply.

I discussed this phenomena last year, albeit without making the recursive link to the monetary system. I'll revisit some of this issue using items from that last post. As far as I know, the concept of a metastasized money supply first came from John Michael Greer in his Archdruid Report, ideas he polished later for his books. From The Economics of Entropy:

. . . (T)here is no such thing as “the” economy in any human society; there are, rather, three economies, each of which follows distinctive rules.

The primary economy, in this way of looking at things, is the natural world itself, which produces something like three-quarters of the goods and services on which human beings rely for survival. The secondary economy, which depends on the primary one, is the collocation of labor, capital plant, and resources extracted from the primary economy that produces the other quarter or so of the goods and services human beings use. The tertiary economy, finally, is the system of social processes by which the products of the first two economies are allocated to people. This can take many different forms, of which the one most familiar to us is money.

Taking out a loan to buy land for farming would use the money to tap the primary economy. Another loan for a tractor taps the secondary. The money itself lies in the tertiary, and as discussed above should be based on the first two levels for the money to have a sense of connection, a sense of value. This limits somewhat how much a bank can theoretically earn, as Nassim Nicholas Taleb notes in his book The Black Swan:

(If) you are in banking and lending, surprise outcomes are likely to be negative for you. You lend, and in the best of circumstances you get your loan back -- but you may lose all of your money if the borrower defaults. In the event that the borrower enjoys great financial success, he is not likely to offer you an additional dividend.

(Nassim Nicholas Taleb, The Black Swan: The Impact of the Highly Improbable, Random House, 2007, pp. 206-207.)

How, then, have banks in recent days managed to accrue such amazing wealth? First, they have developed new tricks. Let's start with a simple, everyday item most of us carry in our wallets: credit cards.

From the commercials extolling the virtues of easy credit, these cards have led to the current prosperity we enjoy today . . . and therefore should not be questioned in any way. Easy credit, though, has not always been the norm in society, as PBS's Frontline exposed in their episode "Secret History of the Credit Card".

From the transcript, we learn that in the 1970s banks were going through very tough times:

NARRATOR: Walter Wriston, then chairman of Citibank, had a credit card division that was hemorrhaging money. New York's usury laws prohibited banks from charging more than 12 percent on most consumer loans.

WALTER WRISTON: Interest rates went up to 20 percent. And if you are lending money at 12 percent and paying 20 percent, you don't have to be Einstein to realize you're out of business.

LOWELL BERGMAN: It was costing Citibank 20 percent for money, and you were only getting 12 percent back?

WALTER WRISTON: Well, sure. Certainly.

LOWELL BERGMAN: Because of the limit on interest.

WALTER WRISTON: There was no way that you could continue.

A Supreme Court decision changed the inevitability of that situation. The Marquette Decision in 1978 determined that "state anti-usury laws regulating interest rates cannot be enforced against nationally-chartered banks based in other states." In other words, if you get a credit card from a bank in one state, the banking and lending laws pertaining to that card are those from the issuing state, even if the card is used primarily in other states. This decision opened the floodgates, according to the former governor of South Dakota:

BILL JANKLOW: The Marquette Bank decision was a U.S. Supreme Court decision that said, forget where the bank is chartered. Wherever the credit decision is made, in whatever state, that's the place where you can apply interest, wherever you make the loan. In other words, if South Dakota had a 25 percent ceiling, then you could charge 25 percent, even to a loan in Florida.

As the Narrator put it in the show, "To get the banks to issue loans, South Dakota decided to eliminate its historic cap on interest rates, known as a usury law" in 1979. Without this historic cap, banks could charge whatever interest rate it wanted on cards issued in South Dakota. Delaware soon followed suit. This greatly increased the financial viability of credit cards. In a few years, cards once so very difficult for individuals to get became more and more common.

Today, the rates, fees and other incidental charges the big banks earn on these cards are one of the most profitable parts of their enterprises. The Frontline piece is a good introduction; I would highly recommend Maxed Out, a documentary that follows the easy credit path down some unexpected directions.

Elizabeth Warren appears in the film. She notes that she was asked to give a speech in front of a group of bankers. Her speech focused on reducing the number of defaults on credit cards and other high-interest loan instruments the banks issued, concluding that denying lower-income people access to easy credit would substantially reduce the number of defaults. As she put it, someone obviously commanding the deference of everyone else in the room -- translation: the boss -- asked a question: Why should they do that when those low-income were the most profitable borrowers the bank had?

The movie also reveals that those cheesy fly-by-night-looking payday loan places dotting the country in strip malls everywhere are actually wholly-owned subsidiaries backed by the major banks. This allows these banks to raise the earnings on the money they lend from reasonable to Holy Shit. I think 750% might be an excessive rate. Furthermore, just like the credit cards and their usurous rates, these places appear to appeal to the lending appetites of those least likely to avoid predatory practices.

Oh, and lest we forget, a credit card purchase also creates money. The cash generated is unsecured -- that is, no collateral is held by the issuing bank to back the loan itself. The banks are taking a big risk with these loans, but as long as more people pay than default, it seems that the profits they make justify that risk. It might also be the reason current legislation recently limited how much credit card debt could be forgiven in the course of a personal bankruptcy.

So now we have, in credit cards and payday loan joints, mechanisms for banks to make some real money. After a few decades of tasting this easy money with little downside, it was time to up the ante.

After the Great Depression of 1929, a series of investigations were started and stopped, culminating with the final investigation under Ferdinand Pecora. His Pecora Commission did some heavy congressional grilling of bankers whose actions, according to the commission's final report (links to a PDF file), were the chief causes of not just the crash of 1929 but by extension the build-up to that crash in the years previous. The legislation acting on Pecora's grilling was called the Banking Act of 1933, otherwise known as the Glass-Steagall Act. As I mentioned in my Open Letter to Adam Davidson: "The Glass-Steagall Act was repealed on November 12, 1999 by the Gramm-Leach-Bliley Act. That giant pool of money started its spectacular, almost tumorous growth in 2000."

I've been mulling a general theory of what led to both the '29 crash and the more recent. I've been perusing the Pecora Report a bit and, by gum, I think I found enough evidence in the report to substantiate my theory. Here goes.

From the Pecora Report, p. 155 (p. 162 of the PDF; the original report does not list the table of content pages, while the PDF does), we learn:

The primary function of commercial banking is to furnish short-term credits for financing the production and distribution of consumable goods. By their nature, such loans should be self-liquidating.

"Self-liquidating" -- what might that mean? Simply, a "short-term" investment should contain clearly defined and agreed-upon terms. A home loan, for example, ends when the principal is paid, whether that occurs at the end of the defined payment schedule, or earlier in the case of an early payoff -- a definition that a stock certificate does not have. One owns a stock certificate until one sells it . . . hopefully at a profit. The Report continues:

A sharp line of demarcation should exist between the function of the commercial banker and the investment banker. Long-term capital financing for the production of "durable goods", such as machinery, railroad equipment, building material, and construction work in general, is the proper field of the investment banker, since such loans are not self-liquidating within the prescribed limits of short-term commercial banking operations.

An investment banker takes private funds and invests them in stocks and other securities; these stocks and securities are in turn used by the issuing companies for the "durable goods" listed in part in that quoted section. It is crucial to note here that an investment bank does not create money through lending.

Combine a commercial bank with an investment bank, however, and that is exactly what could happen . . . and did. From the Pecora Report once again, I'd like to emphasize this section with a screenshot from the PDF:

Remember that the term "credit," as in "flow of credit" and "extension of credit," refers to new money created through loans being used for speculative investment in stocks and securities, instruments whose values fluctuate with market activity. If the value increases, then yes, the bank will make a profit on the transaction. If, however, the value decreases -- or worse, crashes entirely -- then the bank will lose the value underlying the money it issued through the loan. The more money created to speculate, the more the bank had to lose should those speculations prove crashingly wrong.

This money was not lent by any single proscribed method. Rather, the Pecora Report documents many ways that commercial banks funded speculative enterprises. One of the more shocking to me was the issue of loans to employees and officers of the banks directly, without collateral requirements. If you were senior enough or knew the right people, it seemed, you could finance speculation in the stock market. Between pages 185 (PDF 192) and 199 (PDF 206), Pecora outlines several testimonies and provides evidence for several of these schemes, concluding on p. 199 (PDF 206) that:

It has been estimated that approximately 33 percent of the bank failures were substantially contributed to by loans to officers and employees of banks. (I couldn't not emphasize.)

Once again, very few of these loans were "collateralized," meaning, just like credit cards, there was nothing of value behind the money the employees lost for their banks. And it gets better! Pecora states baldly that, in one instance, many employees in one conflict-of-interest loan scandal were still working at their jobs: "At the time of the hearing, February 22, 1933, many of these borrowers were still officers of the bank and affiliated companies." (p. 196 [PDF 203]).

Sound familiar?

So, by loaning money into existence for speculative purposes banks both pre-'29 and today were able to inflame speculation in general, making real money through profitable stock sales in the process. The latest speculative venture lasted a bit longer, it seems. What might have been the difference?

I'm going to continue to speculate. I haven't read the entire Pecora report, after all, and so don't know how specific examples then and now might or might not be related. I do know that there has been an explosion in financial instruments that might have concealed the latest bout of monetary inflation long enough for the subsequent crash to be delayed by a few years.

Take the now-infamous Collateralized Debt Obligation, or CDO, the poster child of the more recent crash. Grab a bunch of home loans, throw them into a CDO and sell it. I won't dwell on this line of financial dumbfuckery. Lots of people are realizing now what an incredibly bad idea it might have been to pay loan officers not by the loans that remain sound, but by the loans they actually get signed. Big conflict of interest there.

Furthermore, let's consider that the more complex a financial instrument the more difficult it might be to decipher what it actually means, let alone determine its value:

National and international securities markets . . . have invented a grammar of options, indexes, and futures that can be applied to different objects of underlying value (often called "underlyings"). At first, these underlyings might be straightforward things like pork bellies, U.S. dollars, or shares of IBM. But when securities markets apply their grammar of options, indexes, and futures to them, new objects of value, often called "derivatives," are created. The markets can then apply the same grammar to these derivatives to create further objects of value in a progressively thickening hierarchy of complexity. In other words, markets recursively apply the same set of rules, over and over again, to the very same things that they have produced through those rules. Some derivatives become so remote from their original underlyings that only the most analytically astute financial managers have any grasp of what they are or mean.

(Thomas Homer-Dixon, The Ingenuity Gap, Alfred A. Knopf, 2000, p. 107, emphasis mine.)

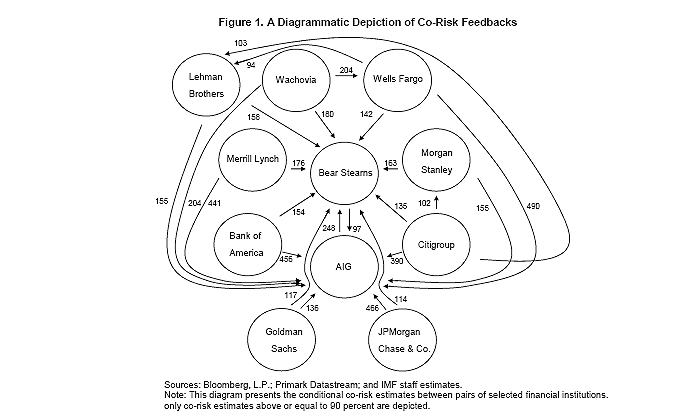

These derivatives might be the number one suspect concealing financial liability. Consider especially the Over-The-Counter derivative. One bank executive goes up to another and says "Hey, you've got a big stock holding on that company and I've got one equally big on this other one. We should "insure" these holdings. I'll give you a few million a year if you agree to give me the value of my holding should it go horribly, horribly bad, and I'll do the same for you. We can then both declare the value both of the money you and I swap and state the value of the payout on our books." I put "insure" in quotes there simply because insurance companies, unlike banks issuing derivatives, have to prove that they have the capital to, well, actually pay their policies, something these banks never thought would be even likely. We all know now that they fucked up. How badly is quite revealing, and something I noted over a year ago:

Each of those lines shows what percentage of the issuing company's assets would be by derivative contract sacrificed to another bank if the entity indicated by the arrow goes under. Look at all those Bear Stearns and AIG arrows.

Dumbfucks. And it gets worse. Where were the regulatory officials during this inflating of the money supply with worthless loans? Well, consider Alan Greenspan. According to Frontline's The Warning, he told Commodities Futures Trading commission head Brooksley Born:

He (Greenspan) said something to the effect that, "Well, Brooksley, we're never going to agree on fraud." And she said, "Well, what do you mean?" And he said, "`You probably think there should be rules against it." And she said, "Well, yes, I do." He said, you know, "I think the market will figure it out and take care of the fraudsters."

The head of the Federal Reserve hates government regulation so much that he thinks some mythical "market" will take care of those that cheat the system. Oh, and it gets worse. At one point in the boom, Greenspan himself tried to slow the growth of money by raising the prime rate just a bit. It didn't have the effect it should have had, probably owing to the easy money speculators could produce from this incestuous relationship between the commercial and investment banks. What did Mr. Greenspan do? Did he make some calls and ask folks why this might be happening? Oh, no. That wouldn't be very libertarian of him, after all. Instead, he scratched his head and decided to let things just happen, without a clue as to what might be causing these anomolies:

"As the historical relationship between measured money supply and spending deteriorated," Greenspan acknowledged, "policy making, seeing no alternative, turned more eclectic and discretionary."

(Homer-Dixon, ibid., p. 296.)

"No alternative?!?" Homer-Dixon continues, stating for all what should have been obvious for Greenspan:

Greenspan's remarks on this and other occasions have been disconcerting. He is at the very pinnacle of economic policy-making, and if he doesn't know how the economic system actually functions, who does? Reading his remarks, one gets the sense that the elite policy-makers at the Federal Reserve are standing on constantly shifting ground, and are repeatedly forced to react to situation "in which incoming data have not readily conformed to historical experience." And because they are often unsure which indicators are most important and deserve most attention, they are in a situation a bit like the one (of the struggling cockpit crew in the damaged plane): they are pushed harder -- their cognitive load is greatly increased -- because they must pay attention to a much wider range of factors than they would if they had a better understanding of the economic system.

(Homer-Dixon, ibid.)

The financial institutions had so drastically "innovated" their businesses -- with commercial/investment banking conflicts of interest, with derivative contracts, with an ever-inflating housing market driven by speculative over-investment at a rampant and almost religious fever -- that the regulatory agencies tasked with overseeing these same businesses had no idea how the traditional indicators related to the state of the economy, and decided instead of acting to let things unfold, to turn "more eclectic and discretionary." Worse, as Nassim Nicholas Taleb notes, it seemed all the major banks had innovated in exactly the same ways, to maximize profits and disregard risk:

We have never lived before under the threat of a global collapse. Financial institutions have been merging into a smaller number of very large banks. Almost all banks are now interrelated. So the financial ecology is swelling into gigantic, incestuous, bureaucratic banks . . . -- when one falls, they all fall. The increased concentration among banks seems to have the effect of making financial crisis less likely, but when they happen they are more global in scale and hit us very hard. We have moved from a diversified ecology of small banks, with varied lending policies, to a more homogeneous framework of firms that all resemble one another. True, we now have fewer failures, but when they occur . . . I shiver at the thought. I rephrase here: we will have fewer but more severe crises. The rarer the event, the less we know about its odds. It mean(s) that we know less and less about the possibility of a crisis.

(Nassim Nicholas Taleb, ibid., pp. 225-226.)

Remember, that book was published in 2006 . . . before the collapse.

Let's get back to the title of this post, "Growth Verses Growths." Both variants of the word "grow" refer to expansion in the money supply. The first refers to "proper" growth of the money supply through prudent lending. In his final report, Pecora quotes Winthrop W. Aldrich, president of the Chase National Bank:

The commercial bank's credit function is very definitely governed by its responsibility to meet its deposit liabilities on demand. . . . Its primary credit function is performed by lending money for short periods to finance self-liquidating commercial transactions, largely in the movement of goods and crops through the various stages of production and distribution; and in the making of short-term loans against good collateral.

(Pecora Report, p. 155 [PDF 162].)

In this way, money is constantly added to the economy, albeit slowly; the collateral required to adequately back this new money must come from either the primary or the secondary economies (again, according to Greer) for the money to be recursively worth something. Yes, as Taleb notes, following this prudent lending path doesn't give banks (or bankers) much profit and exposes them to potentially spectacular losses. That doesn't change the need for prudence and caution.

To use an analogy, imagine that each dollar in our economy corresponds to a body's cell.

Healthy cells in our bodies consume nutrients and contribute to the overall health of the body by using those nutrients to perform a specific task. Some help digest food. Some detect light. Some transmit signals. Some secrete enzymes. Some attack foreign bodies. Some move when told to move. As long as each cell works as it should, it earns its keep.

In a body afflicted with cancer, however, the cancerous cells absorb nutrients but provide no benefit, do no work. Worse, those cells that absorb the most nutrients and replicate the fastest become dominant, leading to an evolutionary race of random mutations that rewards which cell lines will out-compete the others. Eventually, unless the cancer is halted by the body's immune system or treatment, the cancer will absorb too much of the available nutrients and the tasks otherwise performed by the cells will be overlooked, leading to the body's death. The tumor "wins."

When bankers get greedy and try to make lots of money through maximizing methods such as those outlined above -- high-interest and high-fee credit card and "payday loan" lending, funding investment banks with collateral-free loans from commercial banks -- monetary growth metastasizes into growths, into money tumors. Bankers have in their hot profit pursuit confused the dollars they make in profit with dollars that are good for maintaining a sustainable economy; confused sound dollars with unsound. They conflated their product, money, the tertiary economy of their creation -- a creation good only for facilitating the transfer of items in the primary and secondary economies -- as a means unto itself, one that can grow without relation to actual worth.

They have created growths.

Our home market has already collapsed from years of price speculation and inflation. Expect more collapse in prices; until home prices can be afforded by people actually earning a living, they must fall. As economist Herbert Stein noted in his now-famous law: "If something cannot go on forever, it will stop." Prices cannot rise faster than actual purchasing power without being labeled tumorous.

This housing price crisis is not the only crisis coming to a head. It's just the first. Expect also a credit card crisis in the coming years. Very few purchases made with credit cards, after all, have any resale value, any collateral value. Really. Try reselling that double-tall and chocolate-covered biscotti you charged the other day for lunch. It's the reason I've paid off my cards and am paying off monthly balances in full. The same force that drove house values down -- an inability for many to pay -- will probably eventually catch up to the credit card and payday loan industries. The poor can be sued until the lawyers turn blue, but that doesn't mean anyone will be able to pay.

And let's not forget that the primary reason for the Great Depression, the combination of commercial banks with investment banks, has not been addressed by law. It makes me wonder how much of the today's recovery is as inflated, as collateral-free, as illusory as the situation that got us here. Until that obvious conflict of interest between commercial and investment banks is once again rendered illegal, as a country we may never get out of this economic funk.

None of this is good news for anyone, I know.

Sorry.

In this post, I would like to put forth my conjecture about how the current system of loans works fairly well as a back to our money supply, but how several of the largest banks have perverted that system in pursuit of ever greater returns on their money. I ended that last post by demonstrating how a dollar's worth of gold under the gold standard backs a greater amount of paper money. This illustration shows a 6:1 reserve:

The above illustration shows what money was like under the gold standard, a system we no longer follow. Since the latest economic crisis was largely blamed on the housing market, let's replace that coin with a more appropriate symbol:

Let's say you would like to buy this house. You walk into a bank and ask for a home loan. The loan officer reviews (or should review) your ability to pay the bank a regular payment over the next 30 years or so. If you pass this inspection, the bank creates a large pile of money that previous to the loan creation simply didn't exist. With this money you buy the house. In return for the new money, the bank gets an asset; either the loan amount (newly created principal plus interest) or, should you fail to pay as agreed, the foreclosed house. Even if you sell the house before the mortgage is payed in full, the bank gets the principal amount returned.

So, what backs this money? There's no gold, no silver. Critics call this system Fiat money, "fiat" Latin for "let it be done." From the Wiki:

While specie-backed representative money entails the legal requirement that the bank of issue redeem it in fixed weights of specie, fiat money's value is unrelated to the value of any physical quantity. Even a coin containing valuable metal may be considered fiat currency if its face value is higher than its market value as metal.

I italicized that above section because I fundamentally disagree with the Wiki author's declaration. The newly-created money from our speculative scenario is related to a "physical quantity" -- the house.

This might seem endlessly recursive, but only because, well, it is. The value of today's money is pegged to the value of the items held as collateral for the loans that generated the money. In the traditional version of our economic and monetary system, this works pretty well. After all, the homeowner that buys my gray house with the red door does indeed have to pay the mortgage; but he or she avoids the rent that furnished the previous shelter. Owner-occupied homes tend to be maintained better than rentals. (That last sentence is admittedly a bit speculative and based only on my experience living in both environments, predominantly rental neighborhoods and predominantly owner-occupied. A good friend used to have a saying: "Rental; based on the Latin root, to thrash." I would like to see quality-of-life statistics comparing the two types of neighborhoods to either confirm or deny this assertion; but until proven wrong I'm going to stick by this statement.) Thus, I'm going out on a limb and state that densities of predominantly owner-occupied houses raise the value of all the homes in the neighborhood by raising the desirability of the entire neighborhood; furthermore that creating money through loans to create owner-occupied neighborhoods creates real value that supports both the money created and the items procured by that creation.

Let's also remember that loans need not buy only houses. They can also buy equipment for all manner of production, from home construction to factories to software to farms.

I'll say it again: the value of the dollars in our economy is literally in the items bought with the loans that created those dollars. The more closely connected these productive items are to the money produced for their purchase -- the more directly the money that bought these items that "work" to "drive" the myriad activities that produce our food, our shelter, our transportation, our production and our creation -- the stronger both our economy and our monetary system is.

And here we have the problem. What if these items are increasingly distant from the money they support, the money they back, the money created by the loans that bought them? Worse, what if the money created by loans are created for items that have no intrinsic or lasting value? The last thirty years have brought mechanisms to our monetary system that have like a cancer metastasized our money supply.

I discussed this phenomena last year, albeit without making the recursive link to the monetary system. I'll revisit some of this issue using items from that last post. As far as I know, the concept of a metastasized money supply first came from John Michael Greer in his Archdruid Report, ideas he polished later for his books. From The Economics of Entropy:

. . . (T)here is no such thing as “the” economy in any human society; there are, rather, three economies, each of which follows distinctive rules.

The primary economy, in this way of looking at things, is the natural world itself, which produces something like three-quarters of the goods and services on which human beings rely for survival. The secondary economy, which depends on the primary one, is the collocation of labor, capital plant, and resources extracted from the primary economy that produces the other quarter or so of the goods and services human beings use. The tertiary economy, finally, is the system of social processes by which the products of the first two economies are allocated to people. This can take many different forms, of which the one most familiar to us is money.

Taking out a loan to buy land for farming would use the money to tap the primary economy. Another loan for a tractor taps the secondary. The money itself lies in the tertiary, and as discussed above should be based on the first two levels for the money to have a sense of connection, a sense of value. This limits somewhat how much a bank can theoretically earn, as Nassim Nicholas Taleb notes in his book The Black Swan:

(If) you are in banking and lending, surprise outcomes are likely to be negative for you. You lend, and in the best of circumstances you get your loan back -- but you may lose all of your money if the borrower defaults. In the event that the borrower enjoys great financial success, he is not likely to offer you an additional dividend.

(Nassim Nicholas Taleb, The Black Swan: The Impact of the Highly Improbable, Random House, 2007, pp. 206-207.)

How, then, have banks in recent days managed to accrue such amazing wealth? First, they have developed new tricks. Let's start with a simple, everyday item most of us carry in our wallets: credit cards.

From the commercials extolling the virtues of easy credit, these cards have led to the current prosperity we enjoy today . . . and therefore should not be questioned in any way. Easy credit, though, has not always been the norm in society, as PBS's Frontline exposed in their episode "Secret History of the Credit Card".

From the transcript, we learn that in the 1970s banks were going through very tough times:

NARRATOR: Walter Wriston, then chairman of Citibank, had a credit card division that was hemorrhaging money. New York's usury laws prohibited banks from charging more than 12 percent on most consumer loans.

WALTER WRISTON: Interest rates went up to 20 percent. And if you are lending money at 12 percent and paying 20 percent, you don't have to be Einstein to realize you're out of business.

LOWELL BERGMAN: It was costing Citibank 20 percent for money, and you were only getting 12 percent back?

WALTER WRISTON: Well, sure. Certainly.

LOWELL BERGMAN: Because of the limit on interest.

WALTER WRISTON: There was no way that you could continue.

A Supreme Court decision changed the inevitability of that situation. The Marquette Decision in 1978 determined that "state anti-usury laws regulating interest rates cannot be enforced against nationally-chartered banks based in other states." In other words, if you get a credit card from a bank in one state, the banking and lending laws pertaining to that card are those from the issuing state, even if the card is used primarily in other states. This decision opened the floodgates, according to the former governor of South Dakota:

BILL JANKLOW: The Marquette Bank decision was a U.S. Supreme Court decision that said, forget where the bank is chartered. Wherever the credit decision is made, in whatever state, that's the place where you can apply interest, wherever you make the loan. In other words, if South Dakota had a 25 percent ceiling, then you could charge 25 percent, even to a loan in Florida.

As the Narrator put it in the show, "To get the banks to issue loans, South Dakota decided to eliminate its historic cap on interest rates, known as a usury law" in 1979. Without this historic cap, banks could charge whatever interest rate it wanted on cards issued in South Dakota. Delaware soon followed suit. This greatly increased the financial viability of credit cards. In a few years, cards once so very difficult for individuals to get became more and more common.

Today, the rates, fees and other incidental charges the big banks earn on these cards are one of the most profitable parts of their enterprises. The Frontline piece is a good introduction; I would highly recommend Maxed Out, a documentary that follows the easy credit path down some unexpected directions.

Elizabeth Warren appears in the film. She notes that she was asked to give a speech in front of a group of bankers. Her speech focused on reducing the number of defaults on credit cards and other high-interest loan instruments the banks issued, concluding that denying lower-income people access to easy credit would substantially reduce the number of defaults. As she put it, someone obviously commanding the deference of everyone else in the room -- translation: the boss -- asked a question: Why should they do that when those low-income were the most profitable borrowers the bank had?

The movie also reveals that those cheesy fly-by-night-looking payday loan places dotting the country in strip malls everywhere are actually wholly-owned subsidiaries backed by the major banks. This allows these banks to raise the earnings on the money they lend from reasonable to Holy Shit. I think 750% might be an excessive rate. Furthermore, just like the credit cards and their usurous rates, these places appear to appeal to the lending appetites of those least likely to avoid predatory practices.

Oh, and lest we forget, a credit card purchase also creates money. The cash generated is unsecured -- that is, no collateral is held by the issuing bank to back the loan itself. The banks are taking a big risk with these loans, but as long as more people pay than default, it seems that the profits they make justify that risk. It might also be the reason current legislation recently limited how much credit card debt could be forgiven in the course of a personal bankruptcy.

So now we have, in credit cards and payday loan joints, mechanisms for banks to make some real money. After a few decades of tasting this easy money with little downside, it was time to up the ante.

After the Great Depression of 1929, a series of investigations were started and stopped, culminating with the final investigation under Ferdinand Pecora. His Pecora Commission did some heavy congressional grilling of bankers whose actions, according to the commission's final report (links to a PDF file), were the chief causes of not just the crash of 1929 but by extension the build-up to that crash in the years previous. The legislation acting on Pecora's grilling was called the Banking Act of 1933, otherwise known as the Glass-Steagall Act. As I mentioned in my Open Letter to Adam Davidson: "The Glass-Steagall Act was repealed on November 12, 1999 by the Gramm-Leach-Bliley Act. That giant pool of money started its spectacular, almost tumorous growth in 2000."

I've been mulling a general theory of what led to both the '29 crash and the more recent. I've been perusing the Pecora Report a bit and, by gum, I think I found enough evidence in the report to substantiate my theory. Here goes.

From the Pecora Report, p. 155 (p. 162 of the PDF; the original report does not list the table of content pages, while the PDF does), we learn:

The primary function of commercial banking is to furnish short-term credits for financing the production and distribution of consumable goods. By their nature, such loans should be self-liquidating.

"Self-liquidating" -- what might that mean? Simply, a "short-term" investment should contain clearly defined and agreed-upon terms. A home loan, for example, ends when the principal is paid, whether that occurs at the end of the defined payment schedule, or earlier in the case of an early payoff -- a definition that a stock certificate does not have. One owns a stock certificate until one sells it . . . hopefully at a profit. The Report continues:

A sharp line of demarcation should exist between the function of the commercial banker and the investment banker. Long-term capital financing for the production of "durable goods", such as machinery, railroad equipment, building material, and construction work in general, is the proper field of the investment banker, since such loans are not self-liquidating within the prescribed limits of short-term commercial banking operations.

An investment banker takes private funds and invests them in stocks and other securities; these stocks and securities are in turn used by the issuing companies for the "durable goods" listed in part in that quoted section. It is crucial to note here that an investment bank does not create money through lending.

Combine a commercial bank with an investment bank, however, and that is exactly what could happen . . . and did. From the Pecora Report once again, I'd like to emphasize this section with a screenshot from the PDF:

Remember that the term "credit," as in "flow of credit" and "extension of credit," refers to new money created through loans being used for speculative investment in stocks and securities, instruments whose values fluctuate with market activity. If the value increases, then yes, the bank will make a profit on the transaction. If, however, the value decreases -- or worse, crashes entirely -- then the bank will lose the value underlying the money it issued through the loan. The more money created to speculate, the more the bank had to lose should those speculations prove crashingly wrong.

This money was not lent by any single proscribed method. Rather, the Pecora Report documents many ways that commercial banks funded speculative enterprises. One of the more shocking to me was the issue of loans to employees and officers of the banks directly, without collateral requirements. If you were senior enough or knew the right people, it seemed, you could finance speculation in the stock market. Between pages 185 (PDF 192) and 199 (PDF 206), Pecora outlines several testimonies and provides evidence for several of these schemes, concluding on p. 199 (PDF 206) that:

It has been estimated that approximately 33 percent of the bank failures were substantially contributed to by loans to officers and employees of banks. (I couldn't not emphasize.)

Once again, very few of these loans were "collateralized," meaning, just like credit cards, there was nothing of value behind the money the employees lost for their banks. And it gets better! Pecora states baldly that, in one instance, many employees in one conflict-of-interest loan scandal were still working at their jobs: "At the time of the hearing, February 22, 1933, many of these borrowers were still officers of the bank and affiliated companies." (p. 196 [PDF 203]).

Sound familiar?

So, by loaning money into existence for speculative purposes banks both pre-'29 and today were able to inflame speculation in general, making real money through profitable stock sales in the process. The latest speculative venture lasted a bit longer, it seems. What might have been the difference?

I'm going to continue to speculate. I haven't read the entire Pecora report, after all, and so don't know how specific examples then and now might or might not be related. I do know that there has been an explosion in financial instruments that might have concealed the latest bout of monetary inflation long enough for the subsequent crash to be delayed by a few years.

Take the now-infamous Collateralized Debt Obligation, or CDO, the poster child of the more recent crash. Grab a bunch of home loans, throw them into a CDO and sell it. I won't dwell on this line of financial dumbfuckery. Lots of people are realizing now what an incredibly bad idea it might have been to pay loan officers not by the loans that remain sound, but by the loans they actually get signed. Big conflict of interest there.

Furthermore, let's consider that the more complex a financial instrument the more difficult it might be to decipher what it actually means, let alone determine its value:

National and international securities markets . . . have invented a grammar of options, indexes, and futures that can be applied to different objects of underlying value (often called "underlyings"). At first, these underlyings might be straightforward things like pork bellies, U.S. dollars, or shares of IBM. But when securities markets apply their grammar of options, indexes, and futures to them, new objects of value, often called "derivatives," are created. The markets can then apply the same grammar to these derivatives to create further objects of value in a progressively thickening hierarchy of complexity. In other words, markets recursively apply the same set of rules, over and over again, to the very same things that they have produced through those rules. Some derivatives become so remote from their original underlyings that only the most analytically astute financial managers have any grasp of what they are or mean.

(Thomas Homer-Dixon, The Ingenuity Gap, Alfred A. Knopf, 2000, p. 107, emphasis mine.)

These derivatives might be the number one suspect concealing financial liability. Consider especially the Over-The-Counter derivative. One bank executive goes up to another and says "Hey, you've got a big stock holding on that company and I've got one equally big on this other one. We should "insure" these holdings. I'll give you a few million a year if you agree to give me the value of my holding should it go horribly, horribly bad, and I'll do the same for you. We can then both declare the value both of the money you and I swap and state the value of the payout on our books." I put "insure" in quotes there simply because insurance companies, unlike banks issuing derivatives, have to prove that they have the capital to, well, actually pay their policies, something these banks never thought would be even likely. We all know now that they fucked up. How badly is quite revealing, and something I noted over a year ago:

Each of those lines shows what percentage of the issuing company's assets would be by derivative contract sacrificed to another bank if the entity indicated by the arrow goes under. Look at all those Bear Stearns and AIG arrows.

Dumbfucks. And it gets worse. Where were the regulatory officials during this inflating of the money supply with worthless loans? Well, consider Alan Greenspan. According to Frontline's The Warning, he told Commodities Futures Trading commission head Brooksley Born:

He (Greenspan) said something to the effect that, "Well, Brooksley, we're never going to agree on fraud." And she said, "Well, what do you mean?" And he said, "`You probably think there should be rules against it." And she said, "Well, yes, I do." He said, you know, "I think the market will figure it out and take care of the fraudsters."

The head of the Federal Reserve hates government regulation so much that he thinks some mythical "market" will take care of those that cheat the system. Oh, and it gets worse. At one point in the boom, Greenspan himself tried to slow the growth of money by raising the prime rate just a bit. It didn't have the effect it should have had, probably owing to the easy money speculators could produce from this incestuous relationship between the commercial and investment banks. What did Mr. Greenspan do? Did he make some calls and ask folks why this might be happening? Oh, no. That wouldn't be very libertarian of him, after all. Instead, he scratched his head and decided to let things just happen, without a clue as to what might be causing these anomolies:

"As the historical relationship between measured money supply and spending deteriorated," Greenspan acknowledged, "policy making, seeing no alternative, turned more eclectic and discretionary."

(Homer-Dixon, ibid., p. 296.)

"No alternative?!?" Homer-Dixon continues, stating for all what should have been obvious for Greenspan:

Greenspan's remarks on this and other occasions have been disconcerting. He is at the very pinnacle of economic policy-making, and if he doesn't know how the economic system actually functions, who does? Reading his remarks, one gets the sense that the elite policy-makers at the Federal Reserve are standing on constantly shifting ground, and are repeatedly forced to react to situation "in which incoming data have not readily conformed to historical experience." And because they are often unsure which indicators are most important and deserve most attention, they are in a situation a bit like the one (of the struggling cockpit crew in the damaged plane): they are pushed harder -- their cognitive load is greatly increased -- because they must pay attention to a much wider range of factors than they would if they had a better understanding of the economic system.

(Homer-Dixon, ibid.)

The financial institutions had so drastically "innovated" their businesses -- with commercial/investment banking conflicts of interest, with derivative contracts, with an ever-inflating housing market driven by speculative over-investment at a rampant and almost religious fever -- that the regulatory agencies tasked with overseeing these same businesses had no idea how the traditional indicators related to the state of the economy, and decided instead of acting to let things unfold, to turn "more eclectic and discretionary." Worse, as Nassim Nicholas Taleb notes, it seemed all the major banks had innovated in exactly the same ways, to maximize profits and disregard risk:

We have never lived before under the threat of a global collapse. Financial institutions have been merging into a smaller number of very large banks. Almost all banks are now interrelated. So the financial ecology is swelling into gigantic, incestuous, bureaucratic banks . . . -- when one falls, they all fall. The increased concentration among banks seems to have the effect of making financial crisis less likely, but when they happen they are more global in scale and hit us very hard. We have moved from a diversified ecology of small banks, with varied lending policies, to a more homogeneous framework of firms that all resemble one another. True, we now have fewer failures, but when they occur . . . I shiver at the thought. I rephrase here: we will have fewer but more severe crises. The rarer the event, the less we know about its odds. It mean(s) that we know less and less about the possibility of a crisis.

(Nassim Nicholas Taleb, ibid., pp. 225-226.)

Remember, that book was published in 2006 . . . before the collapse.

Let's get back to the title of this post, "Growth Verses Growths." Both variants of the word "grow" refer to expansion in the money supply. The first refers to "proper" growth of the money supply through prudent lending. In his final report, Pecora quotes Winthrop W. Aldrich, president of the Chase National Bank:

The commercial bank's credit function is very definitely governed by its responsibility to meet its deposit liabilities on demand. . . . Its primary credit function is performed by lending money for short periods to finance self-liquidating commercial transactions, largely in the movement of goods and crops through the various stages of production and distribution; and in the making of short-term loans against good collateral.

(Pecora Report, p. 155 [PDF 162].)

In this way, money is constantly added to the economy, albeit slowly; the collateral required to adequately back this new money must come from either the primary or the secondary economies (again, according to Greer) for the money to be recursively worth something. Yes, as Taleb notes, following this prudent lending path doesn't give banks (or bankers) much profit and exposes them to potentially spectacular losses. That doesn't change the need for prudence and caution.

To use an analogy, imagine that each dollar in our economy corresponds to a body's cell.

Healthy cells in our bodies consume nutrients and contribute to the overall health of the body by using those nutrients to perform a specific task. Some help digest food. Some detect light. Some transmit signals. Some secrete enzymes. Some attack foreign bodies. Some move when told to move. As long as each cell works as it should, it earns its keep.

In a body afflicted with cancer, however, the cancerous cells absorb nutrients but provide no benefit, do no work. Worse, those cells that absorb the most nutrients and replicate the fastest become dominant, leading to an evolutionary race of random mutations that rewards which cell lines will out-compete the others. Eventually, unless the cancer is halted by the body's immune system or treatment, the cancer will absorb too much of the available nutrients and the tasks otherwise performed by the cells will be overlooked, leading to the body's death. The tumor "wins."

When bankers get greedy and try to make lots of money through maximizing methods such as those outlined above -- high-interest and high-fee credit card and "payday loan" lending, funding investment banks with collateral-free loans from commercial banks -- monetary growth metastasizes into growths, into money tumors. Bankers have in their hot profit pursuit confused the dollars they make in profit with dollars that are good for maintaining a sustainable economy; confused sound dollars with unsound. They conflated their product, money, the tertiary economy of their creation -- a creation good only for facilitating the transfer of items in the primary and secondary economies -- as a means unto itself, one that can grow without relation to actual worth.

They have created growths.

Our home market has already collapsed from years of price speculation and inflation. Expect more collapse in prices; until home prices can be afforded by people actually earning a living, they must fall. As economist Herbert Stein noted in his now-famous law: "If something cannot go on forever, it will stop." Prices cannot rise faster than actual purchasing power without being labeled tumorous.

This housing price crisis is not the only crisis coming to a head. It's just the first. Expect also a credit card crisis in the coming years. Very few purchases made with credit cards, after all, have any resale value, any collateral value. Really. Try reselling that double-tall and chocolate-covered biscotti you charged the other day for lunch. It's the reason I've paid off my cards and am paying off monthly balances in full. The same force that drove house values down -- an inability for many to pay -- will probably eventually catch up to the credit card and payday loan industries. The poor can be sued until the lawyers turn blue, but that doesn't mean anyone will be able to pay.

And let's not forget that the primary reason for the Great Depression, the combination of commercial banks with investment banks, has not been addressed by law. It makes me wonder how much of the today's recovery is as inflated, as collateral-free, as illusory as the situation that got us here. Until that obvious conflict of interest between commercial and investment banks is once again rendered illegal, as a country we may never get out of this economic funk.

None of this is good news for anyone, I know.

Sorry.