The Myth of the Gold Standard

olego just prompted me to get off my butt. To wit, he saw and liked Secrets of Oz, but noticed the movie pretty much stopped around 1900. True, but that's when Frank Baum published his book. As long as Bill Still called his movie Secrets of Oz, I guess it made sense to stick with the timeline up to the publication.

Still, there is one aspect of the current economic crisis that Baum did not depict through allegory in his book, at least not in any way in which I am familiar, and it's enormously difficult to understand without first understanding how money is created by banks today. I promised some time ago to do a general post on money, and, goaded by olego, here goes. This post will need some graphics. Let's start with the obvious, the foundation of our money:

Let's pretend this is a dollar bill, and that this thing below is a dollar's worth of gold:

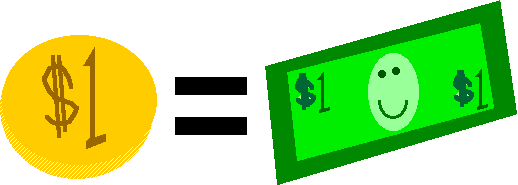

Got that? Good. Now, there are those out there that believe that, in order to repair the damage fiscal irresponsibility has done to our society, we must return to a Gold Standard of money, where each dollar circulating throughout our economy is backed by a dollar's worth of gold held securely in a vault and which can be redeemed by anyone bearing that dollar. This policy can be represented like this:

There's only one problem with this noble and seemingly prudent plan: Not only does the term "Gold Standard" not refer to this one-to-one relationship between paper money and precious metals, this has never been the case. This is something Ellen Hodgeson Brown discussed at length in her book Web of Debt (elements from which I touched on here). To illustrate how the current myth of the Gold Standard may have evolved, let's imagine a world of hundreds of years ago where the printed money actually did represent the amount of gold in a smith's vault . . . because, well, that's kinda how paper money got started.

For our little illustration, let's imagine a goldsmith appropriately named G. Smith. He has a shop in a busy town. He also has the best vault in the city, and rightfully so. It's where he keeps the gold his customers need safely stored. Mr. Smith becomes so well known in his home town, in fact, that one day a customer, Mr. Baker, comes to pick up some gold from his account and asks instead for a note, a scrap of paper signed by Mr. Smith guaranteeing the holder to an amount of gold in the vault deposited by the Mr. Baker. This way Mr. Baker doesn't have to lug the heavy coins through the dangerous roads, the jingling from his coin purse sounding like a dinner bell to would-be cutpurses.

Let's say this note is the start of paper money.

So Mr. Baker leaves the shop with the note and meets Mr. Thatcher. Instead of the filled purse, which Mr. Thatcher had been expecting, he gets only a scrap of paper from Mr. Baker. Still, Thatcher knows Mr. Smith. The shop has been established for generations. The next time he is near Smith's shop, he can redeem the note for the gold.

Or . . . not. As it happens, he owes this amount of gold to Mr. Butcher for the meats to celebrate his daughter's wedding. Why doesn't he just give the note to him, rather than make the trip himself to Mr. Smith's? And Mr. Butcher happens to need the note (or, rather, the money represented by the note) for some supplies he found over at Mr. Chandler's place down by the docks. Chandler himself, later in the week, uses Mr. Smith's note to settle some work he had done at Mr. Cooper's. Hey, those delivery barrels don't build themselves. Cooper needs to pay Mr. Wright for work he had done on his delivery cart, who in turn subsequently needed to pay Mr. Carter for a bunch of deliveries. Finally, needing actual gold -- or probably just to reassure himself that the slip of paper really would be redeemed for coin -- Mr. Carter heads over to Mr. Smith's shop, where Mr. Smith happily gives him what had been -- six bearers of that note in total -- Mr. Baker's money.

Once this system of paper notes got started, it must have been a relief to many. After all, the notes are clearly marked with their value, and not subject to debasing or chipping. (Gold and silver coins were often debased by counterfeiters by mixing the precious metals with baser; sometimes gold content was simply reduced by nipping a bit off the edges off the coin with some snips. That's why today's quarters have those ridges; it's easy to see where the coin was nipped.) Once Mr. Smith invests in a proper press, he can even print his notes, further ensuring the quality of the money he circulates.

Remember, up until now we have assumed Mr. Smith to be a scrupulous and trustworthy keeper of coin. Every time some one needed it, coin would be happily provided in exchange for a Smith Note. People grew to trust Smith. They grew to learn a Smith Note always represented that amount of gold. Until . . . .

Let's say that someone broke into Mr. Smith's vault in the dead of night and made off with all but one-sixth the coin he was storing. The next morning, Mr. Smith learned to his horror that his assets were missing. What would he do?

Well. . . . What if nobody noticed? What if -- other than quietly repairing the vault and upgrading the flaw in security, of course -- Mr. Smith pretended that all was well, that nothing had happened?

Think about this. His practice of circulating paper currency had become well known. Over time, Mr. Smith noticed patterns. Very seldom did notes return directly to the smith's shop. Mr. Baker's coin sat in Mr. Smith's vault for some time, the note representing its value passing hands several times before being redeemed by Mr. Carter. And Mr. Carter might as likely ask for smaller denominations of Smith Notes instead of gold coin, something Smith would be happy in time to provide.

As more and more people grew comfortable with the system, the notes remained longer and longer in circulation, perhaps returning only when they had gotten so worn as to nearly fall apart. At that time, the old notes were simply exchanged by Smith for newer notes of the same denomination and then burned. And the gold? Until the theft, it just sat in the vault, taking up space.

Furthermore, let's remember that those thieves have the coin now, and presumably wish to spend it. Eventually it will be circulated, perhaps to wind up once again in Smith's vault (once he fixed the darned thing). As long as he can pass off the repairs to his customers as just upgrades and not repairs from the theft, there's a good chance no one need be the wiser to his loss, and the gold will once again find itself where it started. His good faith represented by the circulating notes keeps his trusting customers from noticing that there is no longer as much gold in the vault.

It gets better. Now that the thieves are spending their ill-gotten gains, there is more money for everyone. More people are doing business. As long as the money supply doesn't get too large, the economy will grow in proportion to the available supply of money. Previously, people short of either coin or cash would simply barter for their needs directly; with more cash in the economy this barter gets supplanted by more convenient paper notes.

That theft might just convince Mr. Smith never to keep a one-to-one ratio of gold in the vault to paper on the streets.

Which, all fiction aside, is exactly what happened. Goldsmiths were eventually replaced by banks, but banks which learned from the smiths' historic practice. All banks would be started with a private fortune, usually in gold, which would be locked in the vault. Now in business, they would offer two important services, the most obvious security for deposited money. The next was loans. Ellen Brown describes the process:

When you lend someone your own money, your assets go down by the amount that the borrower's assets go up. But when a bank lends you money, its assets go up. Its liabilities also go up, since its deposits are counted as liabilities; but the money isn't really there. It is simply a liability -- something that is owed back to the depositor. The bank turns your promise to pay into an asset and a liability at the same time, balancing its books without actually transferring any pre-existing money to you.

(Ellen Hodgson Brown, Web of Debt, Third Millennium Press, 2008, p. 280.)

In other words, as long as the bank keeps a proper ratio of actual wealth in their vaults -- gold in the old days, other assets today -- they can create money by lending it into existence. That proper ratio is determined by the laws regulating the banks and is called the "fractional reserve." For goldsmiths (according to Brown in an interview), that ratio used to be about 6 to 1, or six dollars of paper circulating for every dollar of gold in the vaults.

Which means we have to revise the Gold Standard illustration somewhat, replacing the equals sign with something a bit more appropriate:

Here the greenish-gold arrow indicates that a buck's worth of gold in reserves allows a bank to create six bucks worth of money.

Of course, no banker would dare create money willy-nilly even within the strictures of the fractional reserve system. No, a proper loan must be backed by adequate collateral and a sound estimate of the borrower's willingness and ability to pay. Otherwise, the banker would be soon go bust.

So, to recap just a bit. Yes, we depositors do give money to our banks for safe keeping and conveniences. That money goes not directly to the borrowers, though, as some (if not most) people assume. Rather, it sits in the vaults and forms part of the reserves against which the bank can create money. The interest the bank pays us for those deposits over time comes from payments on the loans that the bank creates.

I should also add a correction. The illustration shows six dollars created out of a dollar's worth of gold. That was the old fractional reserve requirement based on trial and error. Back in the day, smiths who kept a lower reserve ran the serious risk of running out of specie (gold coin and bullion) and going bankrupt. Today, the actual reserve requirement fluctuates based on what bankers and lawmakers think most prudent. It is not 1-6 (or about 16.6%) anymore.

Today, it's much lower, about 8%. And no gold is required at all.

Y'know, I'm going to go on record and just outright say that I like that we don't use gold anymore. The Gold Standard had its problems.

First of all, let's consider that it's a rare metal. Historically, the population would expand faster than the supply of gold, meaning that a dollar (or pound, or whatever) of gold-backed money would have to service the monetary needs of fewer people. Also, when gold got scarce, those that could hoarded it. Why wouldn't they? It didn't rust away as other metals tend to do. It wasn't eaten by rats. Things that hold their value get hoarded, even if that tended to shorten the money supply and worsen the monetary crisis.

Finally, and most damning, Bill Still in Secrets of Oz points out the numerous bits of historical evidence suggesting bankers have in the past colluded to control the money supply in ways that advanced their own ends, even if it meant society around them suffered as a consequence. Presidents especially who threatened the bankers' monopoly on money tended to suffer for their efforts. Going past 1900, for example, Pres. Franklin D. Roosevelt briefly suspended the gold standard, only to face a plot to surround and seize the White House. Though the plot failed, the Gold Standard was reinstated shortly after this incident.

Ah, but I could wade endlessly into speculation about who controls the real power in this country. Instead, I think I'll end here and take up in another post where I speculate how the bankers abused their power of money creation both leading up to the Great Depression and more recently not in any conspiratorial way, but in a simple move to maximize profits by withholding prudent restraint. Essentially, I intend to show how bankers borrowed themselves to disaster, taking all of us along for the ride.

Still, there is one aspect of the current economic crisis that Baum did not depict through allegory in his book, at least not in any way in which I am familiar, and it's enormously difficult to understand without first understanding how money is created by banks today. I promised some time ago to do a general post on money, and, goaded by olego, here goes. This post will need some graphics. Let's start with the obvious, the foundation of our money:

Let's pretend this is a dollar bill, and that this thing below is a dollar's worth of gold:

Got that? Good. Now, there are those out there that believe that, in order to repair the damage fiscal irresponsibility has done to our society, we must return to a Gold Standard of money, where each dollar circulating throughout our economy is backed by a dollar's worth of gold held securely in a vault and which can be redeemed by anyone bearing that dollar. This policy can be represented like this:

There's only one problem with this noble and seemingly prudent plan: Not only does the term "Gold Standard" not refer to this one-to-one relationship between paper money and precious metals, this has never been the case. This is something Ellen Hodgeson Brown discussed at length in her book Web of Debt (elements from which I touched on here). To illustrate how the current myth of the Gold Standard may have evolved, let's imagine a world of hundreds of years ago where the printed money actually did represent the amount of gold in a smith's vault . . . because, well, that's kinda how paper money got started.

For our little illustration, let's imagine a goldsmith appropriately named G. Smith. He has a shop in a busy town. He also has the best vault in the city, and rightfully so. It's where he keeps the gold his customers need safely stored. Mr. Smith becomes so well known in his home town, in fact, that one day a customer, Mr. Baker, comes to pick up some gold from his account and asks instead for a note, a scrap of paper signed by Mr. Smith guaranteeing the holder to an amount of gold in the vault deposited by the Mr. Baker. This way Mr. Baker doesn't have to lug the heavy coins through the dangerous roads, the jingling from his coin purse sounding like a dinner bell to would-be cutpurses.

Let's say this note is the start of paper money.

So Mr. Baker leaves the shop with the note and meets Mr. Thatcher. Instead of the filled purse, which Mr. Thatcher had been expecting, he gets only a scrap of paper from Mr. Baker. Still, Thatcher knows Mr. Smith. The shop has been established for generations. The next time he is near Smith's shop, he can redeem the note for the gold.

Or . . . not. As it happens, he owes this amount of gold to Mr. Butcher for the meats to celebrate his daughter's wedding. Why doesn't he just give the note to him, rather than make the trip himself to Mr. Smith's? And Mr. Butcher happens to need the note (or, rather, the money represented by the note) for some supplies he found over at Mr. Chandler's place down by the docks. Chandler himself, later in the week, uses Mr. Smith's note to settle some work he had done at Mr. Cooper's. Hey, those delivery barrels don't build themselves. Cooper needs to pay Mr. Wright for work he had done on his delivery cart, who in turn subsequently needed to pay Mr. Carter for a bunch of deliveries. Finally, needing actual gold -- or probably just to reassure himself that the slip of paper really would be redeemed for coin -- Mr. Carter heads over to Mr. Smith's shop, where Mr. Smith happily gives him what had been -- six bearers of that note in total -- Mr. Baker's money.

Once this system of paper notes got started, it must have been a relief to many. After all, the notes are clearly marked with their value, and not subject to debasing or chipping. (Gold and silver coins were often debased by counterfeiters by mixing the precious metals with baser; sometimes gold content was simply reduced by nipping a bit off the edges off the coin with some snips. That's why today's quarters have those ridges; it's easy to see where the coin was nipped.) Once Mr. Smith invests in a proper press, he can even print his notes, further ensuring the quality of the money he circulates.

Remember, up until now we have assumed Mr. Smith to be a scrupulous and trustworthy keeper of coin. Every time some one needed it, coin would be happily provided in exchange for a Smith Note. People grew to trust Smith. They grew to learn a Smith Note always represented that amount of gold. Until . . . .

Let's say that someone broke into Mr. Smith's vault in the dead of night and made off with all but one-sixth the coin he was storing. The next morning, Mr. Smith learned to his horror that his assets were missing. What would he do?

Well. . . . What if nobody noticed? What if -- other than quietly repairing the vault and upgrading the flaw in security, of course -- Mr. Smith pretended that all was well, that nothing had happened?

Think about this. His practice of circulating paper currency had become well known. Over time, Mr. Smith noticed patterns. Very seldom did notes return directly to the smith's shop. Mr. Baker's coin sat in Mr. Smith's vault for some time, the note representing its value passing hands several times before being redeemed by Mr. Carter. And Mr. Carter might as likely ask for smaller denominations of Smith Notes instead of gold coin, something Smith would be happy in time to provide.

As more and more people grew comfortable with the system, the notes remained longer and longer in circulation, perhaps returning only when they had gotten so worn as to nearly fall apart. At that time, the old notes were simply exchanged by Smith for newer notes of the same denomination and then burned. And the gold? Until the theft, it just sat in the vault, taking up space.

Furthermore, let's remember that those thieves have the coin now, and presumably wish to spend it. Eventually it will be circulated, perhaps to wind up once again in Smith's vault (once he fixed the darned thing). As long as he can pass off the repairs to his customers as just upgrades and not repairs from the theft, there's a good chance no one need be the wiser to his loss, and the gold will once again find itself where it started. His good faith represented by the circulating notes keeps his trusting customers from noticing that there is no longer as much gold in the vault.

It gets better. Now that the thieves are spending their ill-gotten gains, there is more money for everyone. More people are doing business. As long as the money supply doesn't get too large, the economy will grow in proportion to the available supply of money. Previously, people short of either coin or cash would simply barter for their needs directly; with more cash in the economy this barter gets supplanted by more convenient paper notes.

That theft might just convince Mr. Smith never to keep a one-to-one ratio of gold in the vault to paper on the streets.

Which, all fiction aside, is exactly what happened. Goldsmiths were eventually replaced by banks, but banks which learned from the smiths' historic practice. All banks would be started with a private fortune, usually in gold, which would be locked in the vault. Now in business, they would offer two important services, the most obvious security for deposited money. The next was loans. Ellen Brown describes the process:

When you lend someone your own money, your assets go down by the amount that the borrower's assets go up. But when a bank lends you money, its assets go up. Its liabilities also go up, since its deposits are counted as liabilities; but the money isn't really there. It is simply a liability -- something that is owed back to the depositor. The bank turns your promise to pay into an asset and a liability at the same time, balancing its books without actually transferring any pre-existing money to you.

(Ellen Hodgson Brown, Web of Debt, Third Millennium Press, 2008, p. 280.)

In other words, as long as the bank keeps a proper ratio of actual wealth in their vaults -- gold in the old days, other assets today -- they can create money by lending it into existence. That proper ratio is determined by the laws regulating the banks and is called the "fractional reserve." For goldsmiths (according to Brown in an interview), that ratio used to be about 6 to 1, or six dollars of paper circulating for every dollar of gold in the vaults.

Which means we have to revise the Gold Standard illustration somewhat, replacing the equals sign with something a bit more appropriate:

Here the greenish-gold arrow indicates that a buck's worth of gold in reserves allows a bank to create six bucks worth of money.

Of course, no banker would dare create money willy-nilly even within the strictures of the fractional reserve system. No, a proper loan must be backed by adequate collateral and a sound estimate of the borrower's willingness and ability to pay. Otherwise, the banker would be soon go bust.

So, to recap just a bit. Yes, we depositors do give money to our banks for safe keeping and conveniences. That money goes not directly to the borrowers, though, as some (if not most) people assume. Rather, it sits in the vaults and forms part of the reserves against which the bank can create money. The interest the bank pays us for those deposits over time comes from payments on the loans that the bank creates.

I should also add a correction. The illustration shows six dollars created out of a dollar's worth of gold. That was the old fractional reserve requirement based on trial and error. Back in the day, smiths who kept a lower reserve ran the serious risk of running out of specie (gold coin and bullion) and going bankrupt. Today, the actual reserve requirement fluctuates based on what bankers and lawmakers think most prudent. It is not 1-6 (or about 16.6%) anymore.

Today, it's much lower, about 8%. And no gold is required at all.

Y'know, I'm going to go on record and just outright say that I like that we don't use gold anymore. The Gold Standard had its problems.

First of all, let's consider that it's a rare metal. Historically, the population would expand faster than the supply of gold, meaning that a dollar (or pound, or whatever) of gold-backed money would have to service the monetary needs of fewer people. Also, when gold got scarce, those that could hoarded it. Why wouldn't they? It didn't rust away as other metals tend to do. It wasn't eaten by rats. Things that hold their value get hoarded, even if that tended to shorten the money supply and worsen the monetary crisis.

Finally, and most damning, Bill Still in Secrets of Oz points out the numerous bits of historical evidence suggesting bankers have in the past colluded to control the money supply in ways that advanced their own ends, even if it meant society around them suffered as a consequence. Presidents especially who threatened the bankers' monopoly on money tended to suffer for their efforts. Going past 1900, for example, Pres. Franklin D. Roosevelt briefly suspended the gold standard, only to face a plot to surround and seize the White House. Though the plot failed, the Gold Standard was reinstated shortly after this incident.

Ah, but I could wade endlessly into speculation about who controls the real power in this country. Instead, I think I'll end here and take up in another post where I speculate how the bankers abused their power of money creation both leading up to the Great Depression and more recently not in any conspiratorial way, but in a simple move to maximize profits by withholding prudent restraint. Essentially, I intend to show how bankers borrowed themselves to disaster, taking all of us along for the ride.