A Fistfull of Greenbacks?

I mentioned a few weeks back that I had finished Douglas Rushkoff's Life, Inc., a book with far too many tantalizing tidbits to share without pretty much transcribing the whole tome. I settled on simply mentioning that teabagger thing. Rushkoff really chronicles not only the rise of the corporation, but also of the monetary system that supports these corporations. Without a centralized money standard, any but small corporations would have difficulty competing with small family businesses.

Why this is the case is fascinating but difficult to explain. Rushkoff mentions that labor and small transactions were at one time traded directly with goods. As the economies of various lands grew, it became efficacious to agree upon a standard medium of exchange, some more or less mutual standard that can be used in lieu of transporting large amounts of commodities for direct barter. For large amounts moved over large distances, royalty used gold, gems and other precious metals.

Tally Sticks from the 13th Century

But for small amounts of value, local economies developed simple tokens that represented a unit of value (wheat from the last harvest or taxes paid). A popular one, used for thousands of years, was the tally stick. I'm almost finished with ellenbrown's Web of Debt, where she discusses this ancient unit of value:

The English tally system originated with King Henry I, son of William the Conqueror, who took the throne in 1100 A.D. The printing press had not yet been invented, and taxes were paid directly with goods produced by the land. Under King Henry's innovative system, payment was recorded with a piece of wood that had been notched and split in half. One half was kept by the government and the other by the recipient. To confirm payment, the two halves were matched to make sure they "tallied." Since no stick splits in an even manner, and since the notches tallying the sums were cut right through both pieces of wood, the method was virtually foolproof against forgery. . . .

Only a few hundred tallies survive . . ., but millions were made. Tallies were used by the government not only as receipts for the payment of taxes but to pay soldiers for their service, farmers for their wheat, and laborers for their labor. . . . By the thirteenth century, the financial market for tallies was sufficiently sophisticated that they could be bought, sold, or discounted. Tallies were used by individuals and institutions to register debts, record fines, collect rents, and enter payments for services rendered. . . . The tally system was thus not a minor monetary experiment, as some commentators have suggested. During most of the Middle Ages, tallies may have made up the bulk of the English money supply. The tally system was in use for more than five centuries before the usury bankers' gold-based paper banknotes took root, helping to fund a long era of leisure and abundance that flowered into the Renaissance.

(Ellen Hodgson Brown, Web of Debt, Third Millennium Press, 2008, p. 59.)

Rushkoff also noted the demise of the tally system as the end of a long and prosperous time. Though remembered today as a somewhat backward time -- Monty Python and the Holy Grail comes to mind -- the Middle Ages were for the lower classes, at least, not so very bad. (Speaking of Python, Terry Jones' Medieval Lives does a good job of dispelling the myths that seemed to accumulate in the 18th and 19th centuries.) An average worker could support himself and his family working only 14 weeks out of the year, for one thing. The rest of the year could be spent on side projects, like pursuing saleable crafts or donating his time to the church to build cathedrals; these were the tourist traps of the Middle Ages, drawing pilgrims and their money to the localities in which they arose.

As gold-based money rose in prominence, though, the old tally system was firmly displaced, a situation that led to the plagues that festered just before and continuing into the Renaissance. Why? Gold tends not to lose value, while the tally system largely pegged value on the most recent harvest. Since a portion of the harvest is later lost to rats, water damage and fire, at the end of a harvest season the older tallies have to be traded in at an adjusted rate for new tallies. Thus the tally holder in these times had every reason to spend his tallies. This age was known, at least amongst the lower classes, as a good time for investment and re-investment in the household and in machinery. Merchants and craftsmen sprang up in villages offering goods and services. The smaller economies thrived as a result.

Things were so prosperous, in fact, that the standing social order was occasionally seen as threatened by, of course, those nearest the top of the order. Jones notes in his documentary a tension between the nobility (those that owned the lands worked by serfs and vassals and to whom the rents on those lands were paid) and these rising merchants. Some nobles even passed laws outlawing the wearing of certain clothing by anyone but nobility. Jones notes that this happened with pointed-toed shoes. Why? The merchants often had more money than the nobles, and would buy the fashionable clothes for themselves, leaving nothing in the clothing styles to denote the difference between those of truly noble birth and what the French call the nouveau riche.

By contrast, gold is scarce. That which is scarce tends to be hoarded. When a society pegs its money on a scarce commodity, the money itself loses what economists call economic velocity -- simply put, the money is not spent as quickly. This can dry up money in the economy. Those economies (like ours) that have no fallback system of barter start to fail. Crops aren't harvested for lack of money to pay farm workers, or for lack of money to simply buy the food after it's brought in. When this started happening near the end of the Middle Ages, Rushkoff notes, plagues started to become more frequent. An impoverished society is a weakened society, literally; people who are not as well-fed fall plague more easily to whatever pestilence happens to be circulating.

Not that the tally sticks are entirely gone from our lives, though, as Brown notes:

Although the tallies were wiped off the books and fell down the memory hole, they left their mark on the modern financial system. The word "stock," meaning financial certificate, comes from the Middle English for the tally stick. . . . The holder of the stock was said to be the "stockholder," who owned "bank stock."

(Brown, ibid, p. 70.)

Yes, the lower classes suffer more when the money supply is reduced. But this suffering often plays into the hands of the upper classes. Those with money can afford to hire, after all. The greater the supply of workers, the more demand placed upon those workers to find a job . . . at any price. Labor becomes a buyer's market.

Meaning those in control of the money supply are in control of the society . . . no matter who is in recognized as the society's actual leaders. Does this necessarily lead to the True Golden Rule, that those who have the gold make the rules? Yes . . . sort of.

Brown's book has gone quite a bit farther than any other I've read at showing what myths perpetuate our current monetary system. It seems, far from being "socialism" or any other left-leaning -ism, government control of the money supply can be a very good thing.

Bear with me. I say that because today, here in the United States, money is created not by the Federal Government, but by banks. This passage puts the situation very succinctly:

When you lend someone your own money, your assets go down by the amount that the borrower's assets go up. But when a bank lends you money, its assets go up. Its liabilities also go up, since its deposits are counted as liabilities; but the money isn't really there. It is simply a liability -- something that is owed back to the depositor. The bank turns your promise to pay into an asset and a liability at the same time, balancing its books without actually transferring any pre-existing money to you.

(Brown, ibid, p. 280, emphasis by the author.)

". . . the money isn't really there." Let that sink in for a bit. In example after example, Web of Debt demonstrates how the creation of dollars is a simple accounting exercise. Dollars are created by demand every time a loan is made. These dollars don't exist except as entries in the bank's ledgers. It is our faith that these newly-created dollars are backed by piles of gold in the vaults or the full faith and credit of the United States Government that gives them value.

So, in times of inflation, the banks are in control and are therefore responsible, not the mythical out-of-control printing presses supposedly put to work by Congress. Congress, the President, all of our elected leaders, actually have very little to say about what happens in our economy. You can vote the bastards out all you want, but they aren't the problem.

At least, that's the case today. It hasn't always been the case.

Before the American Revolution, Benjamin Franklin journeyed to London to petition the King over concerns faced by the colonists. He was shocked by the poverty he witnessed, the filled poor houses, legions of unemployed and beggars on the street. England was by that time well distanced from the tally sticks and firmly on the gold standard. Londoners asked Franklin how the colonies take care of their unemployed and destitute. He declared that they didn't have any. When asked how this could be, he wrote:

That is simple. In the colonies we issue our own money. It is called Colonial Scrip. We issue it to pay the government's approved expenses and charities. We make sure it is issued in proper proportions to make the goods pass easily from the producers to the consumers. . . . In this manner, creating for ourselves our own paper money, we control its purchasing power, and we have no interest to pay to no one. You see, a legitimate government can both spend and lend money into circulation, while banks can only lend significant amounts of their promissory bank notes, for they can neither give away nor spend but a tiny fraction of the money the people need. Thus when your bankers here in England place money in circulation, there is always a debt principal to be returned and usury to be paid. The result is that you have always too little credit in circulation to give the workers full employment. You do not have too many workers, you have too little money in circulation, and that which circulates, all bears the endless burden of unpayable debt and usury.

(Brown, ibid, pp. 40-41, emphasis by the author.)

Brown further maintains that deprivations caused by King George's subsequent outlawing of colonial currency -- the very currency that kept the colonial government thriving without gold -- led eventually to the Revolution.

In later years, Franklin tutored a young man named Matthew Carey. His experience must have passed to Matthew, for Matthew's son Henry later became President Abraham Lincoln's chief financial adviser. This is key to understanding what Lincoln did to fund the Union's fight in the Civil War:

Lincoln tapped into the same cornerstone that had gotten the impoverished colonists through the American Revolution and a long period of internal development before that: he authorized the government to issue its own paper fiat money. National control was reestablished over banking, and the economy was jump-started with a 600 percent increase in government spending and cheap credit directed at production. . . . Officially called United States Notes, these nineteenth century tallies were popularly called "Greenbacks" because they were printed on the back with green ink (a feature the dollar retains today). They were basically just receipts acknowledging work done or goods delivered, which could be traded in the community for an equivalent value of goods or services. The Greenbacks represented man-hours rather than borrowed gold. Lincoln is quoted as saying, "The wages of men should be recognized as more important than the wages of money."

(Brown, ibid, pp. 82-83.)

Lincoln was, of course, later assassinated. The country eventually returned to the gold standard for its money under an Act called by many "the crime of 1873." The prosperity following the Civil War fell into crisis after crisis. Describing this era, the whole of Brown's book can be distilled in one early passage:

Money reform advocates today tend to argue that the solution to the country's financial woes is to return to the "gold standard," which required that paper money be backed by a certain weight of gold bullion. But to the farmers and laborers who were suffering under its yoke in the 1890s, the gold standard was the problem. They had been there and knew it didn't work. William Jennings Bryan called the banker's private gold-based money a "cross of gold." There was simply not enough gold available to finance the needs of an expanding economy. The bankers made loans in notes backed by gold and required repayment in notes backed by gold; but the bankers controlled the gold, and its price was subject to manipulation by speculators. . . . People short of gold had to borrow from the bankers, who periodically contracted the money supply by calling in loans and raising interest rates. The result was "tight" money -- insufficient money to go around. Like in a game of musical chairs, the people who came up short wound up losing their homes to the banks.

(Brown, ibid, pp. 13-14.)

I've given you two prominent examples from US history that defies the common wisdom that governments can't be trusted with the printing presses without devaluing the resulting currency and plunging the country into financial chaos. Let me continue by giving you more, just in case you are yet unconvinced.

Burning marks for heat.

Many have by now heard of what happened to Germany under the Weimar regime, how hyperinflation ran so rampant that a wheelbarrow of cash couldn't buy a loaf of bread, or the cost of coal for heat is less than just burning the money. I've added this link so you can scroll down and look at the pictures; keep in mind that the economic opinions expressed in the linked article itself, according to Brown, is complete bullshit. From the link:

Almost all economists and politicians in power are Keynesian economists. They believe the free market is chaotic, illogical, and inefficient. They believe they are smarter than the market. They believe they can prevent the cycles of boom and bust. The founder of this type of economic thinking is John Maynard Keynes. He famously proclaimed “We will not have any more crashes in our time.” in 1927 (years before the Great Depression).

The result of these Keynesian policies is inflation. Inflation is a tool used to transfer wealth from producers to worthless bureaucrats and their pet projects. As the government becomes more desperate for cash, they will increase the flow of paper money (fiat currency) until the entire financial system becomes insoluble. As the American dollar weakens, foreign countries will sell their bonds and flood the market with devalued currency. You can expect inflation like the U.S. has never experienced. The cost of items will skyrocket and your wages will stay the same. Those in power will blame the free market and capitalism but the real cause of the fall will be their failed economic policies.

According to Brown, once again, this is bullshit, either deliberate or unintentional. (Judging only by the quality of the writing, I'm leaning to the latter, but admittedly don't know for sure.) It turns out that the Reichsbank marks were being manipulated by foreign banking interests, perhaps for profit, or perhaps to keep Germany poor:

Like the U.S. Federal Reserve, the Reichsbank was overseen by appointed government officials but was operated for private gain. The mark's dramatic devaluation began soon after the Reichsbank was "privatized," or delivered to private investors. What drove the wartime inflation into hyperinflation . . . was speculation by foreign investors, who would sell the mark short, betting on its decreasing value. Recall that in the short sale, speculators borrow something they don't own, sell it, then "cover" by buying it back at the lower price. Speculation in the German mark was made possible because the Reichsbank made massive amounts of currency available for borrowing, marks that were created on demand and lent at a profitable interest to the bank. When the Reichsbank could not keep up with the voracious demand for marks, other private banks were allowed to create them out of nothing and lend them at interest as well.

(Brown, ibid, p. 233.)

"Short Selling" really needs to be explained. In a short sale, someone brings an asset to market that he doesn't own. He can borrow it or -- worse -- just pretend to have it. He walks into the market and proclaims a desire to sell it at a very low price. This happens legitimately when someone needs money quickly. Sellers snap up that asset as quickly as possible. After the sale, the posted price of that asset will fall relative to the previous prices. If enough of the asset is unloaded, or if bad information about the asset is circulated (who would do that? hint, hint, nudge nudge), others may unload their assets as well, further dropping the price. After enough of the asset's price has been shed, the original seller buys the asset back at that lower price. The difference between the original fire sale price and the repurchase price is pure profit.

It gets worse in the "naked short sell;" here the seller doesn't even own the asset being sold. I'll let Brown describe one especially egregious example:

A story run on FinancialWire in March 2005 underscored the pervasiveness of naked short selling. A man named Robert Simpson purchased all of the outstanding stock of a small comany called Global Links Corporation, totaling a little over one million shares. He put all of this stock in his sock drawer, then watched as 60 million of the company's shares traded hands over the next two days. . . . The incident substantiated allegation that a staggering number of "phantom" shares are being traded around by brokers in naked short sales. Short sellers are expected to "cover" by buying back the stock and returning it to the pool, but Simpson's 60 million shares were obviously never bought back, since they were not available for purchase. . . .

(Brown, ibid, p. 183, emphasis by the author.)

Stocks trade just like currencies allowed to "float," or available to exchange for other currencies for whatever the market will pay. The same process that devalued stocks over the years in short sales too numerous to count have devalued the currencies of nations . . . on which the people of these nations rely for their economic well-being. To continue with what happened to Germany:

The German people were in such desperate straits that they relinquished control of the country to a dictator. . . . But autocratic authority did give Adolf Hitler something the American Greenbackers could only dream about -- total control of the economy. He was able to test their theories, and he proved that they worked. Like for Lincoln, Hitler's choices were to either submit to total debt slavery or create his own fiat money; and like Lincoln, he chose the fiat solution. . . .

Within two years, the unemployment problem had been solved and the country was back on its feet. It had a solid, stable currency and no inflation, at a time when millions of people in the United States and other Western countries were still out of work and living on welfare. Germany even managed to restore foreign trade . . . using a barter system: equipment and commodities were exchanged directly with other countries, circumventing the international banks. This system of direct exchange occurred without debt and without trade deficits. Germany's economic experiment, like Lincoln's, was short-lived; but it left some lasting monuments to its success, including the famous Autobahn, the world's first extensive superhighway.

(Brown, ibid, p. 230.)

Germany went from scenes of burning money for heat to prosperity. Within two years. With this in mind, is the lavishing praise Germans had for Hitler so surprising? Yes, it led to an enormous amount of strife as he ordered acts for which he is far better known; but two years?!? I'm not sure I wouldn't be able to resist the charms of a public figure who accomplished such a feat. Amazing. And, let's remember, he did it by enacting strict Lincoln-esque government control of the currency, not by freeing it to market forces.

I've not been lighting your eyeballs until now just to praise Brown for her book. I came across Brown and her ideas some time ago when kmo interviewed her for his C-Realm Podcast. Well, he's had another C-Realm guest of note, Nathan A. Martin, interviewed in Episode 199: Velocity & Saturation. Martin takes Brown's ideas, as Nigel of Spinal Tap might say, to 11.

Martin has founded Swarm USA, an attempt to decouple our monetary system from the direct control of banks. Like Brown, he notes that, though we as a country have not been on the gold standard for some years, the process that creates deficit money creates the need to pay interest to the banks when it is created . . . interest that has been accumulating for a number of years. Accumulating, and compounding. Martin notes here that "the real amount of money spent on interest last year alone nearly equals the total amount of money our government takes in!"

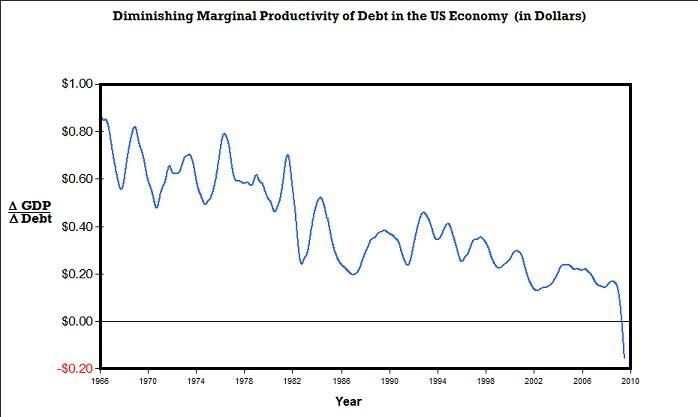

He maintains that we have reached "debt saturation." That is, the cost of paying down the historic debt has gotten so large that borrowing more money from the Federal Reserve (remember, a collection of privately-owned banks, not a branch of the government) will actually decrease the amount of money in our economy.

Specifically, according to this chart from his site, every new dollar added to the economy carries enough debt to actually suck $.15 out of circulation. If true, we are looking at a prolonged recession the likes of which may never have been seen in this country.

I admit it: I'm no economist. I'm no expert. I did, though, want you folks out there to take a look at the links and information I've provided to see if you can make heads or tails out of it. Sadly, it seems to fit the available information. With enough cash, one can short sell currencies that float relative to others. With enough debt, the burden can grow large enough to become onerous, as evidenced by the massive wave of foreclosures that followed the sub-prime mortgage peak. According once again to Martin, who quotes the Treasury Dept. in the linked site, last year Treasury spent more on paying interest on currency than it spent on Defense, a statistic that puts mere homeowners underwater on their house to shame.

I'll continue to look at this stuff, and welcome your input. Right now, though, it's dinner time.

Addendum, The Next Day: alobar pointed out that the extreme haste of posting on an empty stomach hath weakened my words. I noticed many other goofs, such as the omission of the short sale description, and have amended.

Addendum, June 7, 2010: More goofs corrected. Misspellings this time.

Why this is the case is fascinating but difficult to explain. Rushkoff mentions that labor and small transactions were at one time traded directly with goods. As the economies of various lands grew, it became efficacious to agree upon a standard medium of exchange, some more or less mutual standard that can be used in lieu of transporting large amounts of commodities for direct barter. For large amounts moved over large distances, royalty used gold, gems and other precious metals.

Tally Sticks from the 13th Century

But for small amounts of value, local economies developed simple tokens that represented a unit of value (wheat from the last harvest or taxes paid). A popular one, used for thousands of years, was the tally stick. I'm almost finished with ellenbrown's Web of Debt, where she discusses this ancient unit of value:

The English tally system originated with King Henry I, son of William the Conqueror, who took the throne in 1100 A.D. The printing press had not yet been invented, and taxes were paid directly with goods produced by the land. Under King Henry's innovative system, payment was recorded with a piece of wood that had been notched and split in half. One half was kept by the government and the other by the recipient. To confirm payment, the two halves were matched to make sure they "tallied." Since no stick splits in an even manner, and since the notches tallying the sums were cut right through both pieces of wood, the method was virtually foolproof against forgery. . . .

Only a few hundred tallies survive . . ., but millions were made. Tallies were used by the government not only as receipts for the payment of taxes but to pay soldiers for their service, farmers for their wheat, and laborers for their labor. . . . By the thirteenth century, the financial market for tallies was sufficiently sophisticated that they could be bought, sold, or discounted. Tallies were used by individuals and institutions to register debts, record fines, collect rents, and enter payments for services rendered. . . . The tally system was thus not a minor monetary experiment, as some commentators have suggested. During most of the Middle Ages, tallies may have made up the bulk of the English money supply. The tally system was in use for more than five centuries before the usury bankers' gold-based paper banknotes took root, helping to fund a long era of leisure and abundance that flowered into the Renaissance.

(Ellen Hodgson Brown, Web of Debt, Third Millennium Press, 2008, p. 59.)

Rushkoff also noted the demise of the tally system as the end of a long and prosperous time. Though remembered today as a somewhat backward time -- Monty Python and the Holy Grail comes to mind -- the Middle Ages were for the lower classes, at least, not so very bad. (Speaking of Python, Terry Jones' Medieval Lives does a good job of dispelling the myths that seemed to accumulate in the 18th and 19th centuries.) An average worker could support himself and his family working only 14 weeks out of the year, for one thing. The rest of the year could be spent on side projects, like pursuing saleable crafts or donating his time to the church to build cathedrals; these were the tourist traps of the Middle Ages, drawing pilgrims and their money to the localities in which they arose.

As gold-based money rose in prominence, though, the old tally system was firmly displaced, a situation that led to the plagues that festered just before and continuing into the Renaissance. Why? Gold tends not to lose value, while the tally system largely pegged value on the most recent harvest. Since a portion of the harvest is later lost to rats, water damage and fire, at the end of a harvest season the older tallies have to be traded in at an adjusted rate for new tallies. Thus the tally holder in these times had every reason to spend his tallies. This age was known, at least amongst the lower classes, as a good time for investment and re-investment in the household and in machinery. Merchants and craftsmen sprang up in villages offering goods and services. The smaller economies thrived as a result.

Things were so prosperous, in fact, that the standing social order was occasionally seen as threatened by, of course, those nearest the top of the order. Jones notes in his documentary a tension between the nobility (those that owned the lands worked by serfs and vassals and to whom the rents on those lands were paid) and these rising merchants. Some nobles even passed laws outlawing the wearing of certain clothing by anyone but nobility. Jones notes that this happened with pointed-toed shoes. Why? The merchants often had more money than the nobles, and would buy the fashionable clothes for themselves, leaving nothing in the clothing styles to denote the difference between those of truly noble birth and what the French call the nouveau riche.

By contrast, gold is scarce. That which is scarce tends to be hoarded. When a society pegs its money on a scarce commodity, the money itself loses what economists call economic velocity -- simply put, the money is not spent as quickly. This can dry up money in the economy. Those economies (like ours) that have no fallback system of barter start to fail. Crops aren't harvested for lack of money to pay farm workers, or for lack of money to simply buy the food after it's brought in. When this started happening near the end of the Middle Ages, Rushkoff notes, plagues started to become more frequent. An impoverished society is a weakened society, literally; people who are not as well-fed fall plague more easily to whatever pestilence happens to be circulating.

Not that the tally sticks are entirely gone from our lives, though, as Brown notes:

Although the tallies were wiped off the books and fell down the memory hole, they left their mark on the modern financial system. The word "stock," meaning financial certificate, comes from the Middle English for the tally stick. . . . The holder of the stock was said to be the "stockholder," who owned "bank stock."

(Brown, ibid, p. 70.)

Yes, the lower classes suffer more when the money supply is reduced. But this suffering often plays into the hands of the upper classes. Those with money can afford to hire, after all. The greater the supply of workers, the more demand placed upon those workers to find a job . . . at any price. Labor becomes a buyer's market.

Meaning those in control of the money supply are in control of the society . . . no matter who is in recognized as the society's actual leaders. Does this necessarily lead to the True Golden Rule, that those who have the gold make the rules? Yes . . . sort of.

Brown's book has gone quite a bit farther than any other I've read at showing what myths perpetuate our current monetary system. It seems, far from being "socialism" or any other left-leaning -ism, government control of the money supply can be a very good thing.

Bear with me. I say that because today, here in the United States, money is created not by the Federal Government, but by banks. This passage puts the situation very succinctly:

When you lend someone your own money, your assets go down by the amount that the borrower's assets go up. But when a bank lends you money, its assets go up. Its liabilities also go up, since its deposits are counted as liabilities; but the money isn't really there. It is simply a liability -- something that is owed back to the depositor. The bank turns your promise to pay into an asset and a liability at the same time, balancing its books without actually transferring any pre-existing money to you.

(Brown, ibid, p. 280, emphasis by the author.)

". . . the money isn't really there." Let that sink in for a bit. In example after example, Web of Debt demonstrates how the creation of dollars is a simple accounting exercise. Dollars are created by demand every time a loan is made. These dollars don't exist except as entries in the bank's ledgers. It is our faith that these newly-created dollars are backed by piles of gold in the vaults or the full faith and credit of the United States Government that gives them value.

So, in times of inflation, the banks are in control and are therefore responsible, not the mythical out-of-control printing presses supposedly put to work by Congress. Congress, the President, all of our elected leaders, actually have very little to say about what happens in our economy. You can vote the bastards out all you want, but they aren't the problem.

At least, that's the case today. It hasn't always been the case.

Before the American Revolution, Benjamin Franklin journeyed to London to petition the King over concerns faced by the colonists. He was shocked by the poverty he witnessed, the filled poor houses, legions of unemployed and beggars on the street. England was by that time well distanced from the tally sticks and firmly on the gold standard. Londoners asked Franklin how the colonies take care of their unemployed and destitute. He declared that they didn't have any. When asked how this could be, he wrote:

That is simple. In the colonies we issue our own money. It is called Colonial Scrip. We issue it to pay the government's approved expenses and charities. We make sure it is issued in proper proportions to make the goods pass easily from the producers to the consumers. . . . In this manner, creating for ourselves our own paper money, we control its purchasing power, and we have no interest to pay to no one. You see, a legitimate government can both spend and lend money into circulation, while banks can only lend significant amounts of their promissory bank notes, for they can neither give away nor spend but a tiny fraction of the money the people need. Thus when your bankers here in England place money in circulation, there is always a debt principal to be returned and usury to be paid. The result is that you have always too little credit in circulation to give the workers full employment. You do not have too many workers, you have too little money in circulation, and that which circulates, all bears the endless burden of unpayable debt and usury.

(Brown, ibid, pp. 40-41, emphasis by the author.)

Brown further maintains that deprivations caused by King George's subsequent outlawing of colonial currency -- the very currency that kept the colonial government thriving without gold -- led eventually to the Revolution.

In later years, Franklin tutored a young man named Matthew Carey. His experience must have passed to Matthew, for Matthew's son Henry later became President Abraham Lincoln's chief financial adviser. This is key to understanding what Lincoln did to fund the Union's fight in the Civil War:

Lincoln tapped into the same cornerstone that had gotten the impoverished colonists through the American Revolution and a long period of internal development before that: he authorized the government to issue its own paper fiat money. National control was reestablished over banking, and the economy was jump-started with a 600 percent increase in government spending and cheap credit directed at production. . . . Officially called United States Notes, these nineteenth century tallies were popularly called "Greenbacks" because they were printed on the back with green ink (a feature the dollar retains today). They were basically just receipts acknowledging work done or goods delivered, which could be traded in the community for an equivalent value of goods or services. The Greenbacks represented man-hours rather than borrowed gold. Lincoln is quoted as saying, "The wages of men should be recognized as more important than the wages of money."

(Brown, ibid, pp. 82-83.)

Lincoln was, of course, later assassinated. The country eventually returned to the gold standard for its money under an Act called by many "the crime of 1873." The prosperity following the Civil War fell into crisis after crisis. Describing this era, the whole of Brown's book can be distilled in one early passage:

Money reform advocates today tend to argue that the solution to the country's financial woes is to return to the "gold standard," which required that paper money be backed by a certain weight of gold bullion. But to the farmers and laborers who were suffering under its yoke in the 1890s, the gold standard was the problem. They had been there and knew it didn't work. William Jennings Bryan called the banker's private gold-based money a "cross of gold." There was simply not enough gold available to finance the needs of an expanding economy. The bankers made loans in notes backed by gold and required repayment in notes backed by gold; but the bankers controlled the gold, and its price was subject to manipulation by speculators. . . . People short of gold had to borrow from the bankers, who periodically contracted the money supply by calling in loans and raising interest rates. The result was "tight" money -- insufficient money to go around. Like in a game of musical chairs, the people who came up short wound up losing their homes to the banks.

(Brown, ibid, pp. 13-14.)

I've given you two prominent examples from US history that defies the common wisdom that governments can't be trusted with the printing presses without devaluing the resulting currency and plunging the country into financial chaos. Let me continue by giving you more, just in case you are yet unconvinced.

Burning marks for heat.

Many have by now heard of what happened to Germany under the Weimar regime, how hyperinflation ran so rampant that a wheelbarrow of cash couldn't buy a loaf of bread, or the cost of coal for heat is less than just burning the money. I've added this link so you can scroll down and look at the pictures; keep in mind that the economic opinions expressed in the linked article itself, according to Brown, is complete bullshit. From the link:

Almost all economists and politicians in power are Keynesian economists. They believe the free market is chaotic, illogical, and inefficient. They believe they are smarter than the market. They believe they can prevent the cycles of boom and bust. The founder of this type of economic thinking is John Maynard Keynes. He famously proclaimed “We will not have any more crashes in our time.” in 1927 (years before the Great Depression).

The result of these Keynesian policies is inflation. Inflation is a tool used to transfer wealth from producers to worthless bureaucrats and their pet projects. As the government becomes more desperate for cash, they will increase the flow of paper money (fiat currency) until the entire financial system becomes insoluble. As the American dollar weakens, foreign countries will sell their bonds and flood the market with devalued currency. You can expect inflation like the U.S. has never experienced. The cost of items will skyrocket and your wages will stay the same. Those in power will blame the free market and capitalism but the real cause of the fall will be their failed economic policies.

According to Brown, once again, this is bullshit, either deliberate or unintentional. (Judging only by the quality of the writing, I'm leaning to the latter, but admittedly don't know for sure.) It turns out that the Reichsbank marks were being manipulated by foreign banking interests, perhaps for profit, or perhaps to keep Germany poor:

Like the U.S. Federal Reserve, the Reichsbank was overseen by appointed government officials but was operated for private gain. The mark's dramatic devaluation began soon after the Reichsbank was "privatized," or delivered to private investors. What drove the wartime inflation into hyperinflation . . . was speculation by foreign investors, who would sell the mark short, betting on its decreasing value. Recall that in the short sale, speculators borrow something they don't own, sell it, then "cover" by buying it back at the lower price. Speculation in the German mark was made possible because the Reichsbank made massive amounts of currency available for borrowing, marks that were created on demand and lent at a profitable interest to the bank. When the Reichsbank could not keep up with the voracious demand for marks, other private banks were allowed to create them out of nothing and lend them at interest as well.

(Brown, ibid, p. 233.)

"Short Selling" really needs to be explained. In a short sale, someone brings an asset to market that he doesn't own. He can borrow it or -- worse -- just pretend to have it. He walks into the market and proclaims a desire to sell it at a very low price. This happens legitimately when someone needs money quickly. Sellers snap up that asset as quickly as possible. After the sale, the posted price of that asset will fall relative to the previous prices. If enough of the asset is unloaded, or if bad information about the asset is circulated (who would do that? hint, hint, nudge nudge), others may unload their assets as well, further dropping the price. After enough of the asset's price has been shed, the original seller buys the asset back at that lower price. The difference between the original fire sale price and the repurchase price is pure profit.

It gets worse in the "naked short sell;" here the seller doesn't even own the asset being sold. I'll let Brown describe one especially egregious example:

A story run on FinancialWire in March 2005 underscored the pervasiveness of naked short selling. A man named Robert Simpson purchased all of the outstanding stock of a small comany called Global Links Corporation, totaling a little over one million shares. He put all of this stock in his sock drawer, then watched as 60 million of the company's shares traded hands over the next two days. . . . The incident substantiated allegation that a staggering number of "phantom" shares are being traded around by brokers in naked short sales. Short sellers are expected to "cover" by buying back the stock and returning it to the pool, but Simpson's 60 million shares were obviously never bought back, since they were not available for purchase. . . .

(Brown, ibid, p. 183, emphasis by the author.)

Stocks trade just like currencies allowed to "float," or available to exchange for other currencies for whatever the market will pay. The same process that devalued stocks over the years in short sales too numerous to count have devalued the currencies of nations . . . on which the people of these nations rely for their economic well-being. To continue with what happened to Germany:

The German people were in such desperate straits that they relinquished control of the country to a dictator. . . . But autocratic authority did give Adolf Hitler something the American Greenbackers could only dream about -- total control of the economy. He was able to test their theories, and he proved that they worked. Like for Lincoln, Hitler's choices were to either submit to total debt slavery or create his own fiat money; and like Lincoln, he chose the fiat solution. . . .

Within two years, the unemployment problem had been solved and the country was back on its feet. It had a solid, stable currency and no inflation, at a time when millions of people in the United States and other Western countries were still out of work and living on welfare. Germany even managed to restore foreign trade . . . using a barter system: equipment and commodities were exchanged directly with other countries, circumventing the international banks. This system of direct exchange occurred without debt and without trade deficits. Germany's economic experiment, like Lincoln's, was short-lived; but it left some lasting monuments to its success, including the famous Autobahn, the world's first extensive superhighway.

(Brown, ibid, p. 230.)

Germany went from scenes of burning money for heat to prosperity. Within two years. With this in mind, is the lavishing praise Germans had for Hitler so surprising? Yes, it led to an enormous amount of strife as he ordered acts for which he is far better known; but two years?!? I'm not sure I wouldn't be able to resist the charms of a public figure who accomplished such a feat. Amazing. And, let's remember, he did it by enacting strict Lincoln-esque government control of the currency, not by freeing it to market forces.

I've not been lighting your eyeballs until now just to praise Brown for her book. I came across Brown and her ideas some time ago when kmo interviewed her for his C-Realm Podcast. Well, he's had another C-Realm guest of note, Nathan A. Martin, interviewed in Episode 199: Velocity & Saturation. Martin takes Brown's ideas, as Nigel of Spinal Tap might say, to 11.

Martin has founded Swarm USA, an attempt to decouple our monetary system from the direct control of banks. Like Brown, he notes that, though we as a country have not been on the gold standard for some years, the process that creates deficit money creates the need to pay interest to the banks when it is created . . . interest that has been accumulating for a number of years. Accumulating, and compounding. Martin notes here that "the real amount of money spent on interest last year alone nearly equals the total amount of money our government takes in!"

He maintains that we have reached "debt saturation." That is, the cost of paying down the historic debt has gotten so large that borrowing more money from the Federal Reserve (remember, a collection of privately-owned banks, not a branch of the government) will actually decrease the amount of money in our economy.

Specifically, according to this chart from his site, every new dollar added to the economy carries enough debt to actually suck $.15 out of circulation. If true, we are looking at a prolonged recession the likes of which may never have been seen in this country.

I admit it: I'm no economist. I'm no expert. I did, though, want you folks out there to take a look at the links and information I've provided to see if you can make heads or tails out of it. Sadly, it seems to fit the available information. With enough cash, one can short sell currencies that float relative to others. With enough debt, the burden can grow large enough to become onerous, as evidenced by the massive wave of foreclosures that followed the sub-prime mortgage peak. According once again to Martin, who quotes the Treasury Dept. in the linked site, last year Treasury spent more on paying interest on currency than it spent on Defense, a statistic that puts mere homeowners underwater on their house to shame.

I'll continue to look at this stuff, and welcome your input. Right now, though, it's dinner time.

Addendum, The Next Day: alobar pointed out that the extreme haste of posting on an empty stomach hath weakened my words. I noticed many other goofs, such as the omission of the short sale description, and have amended.

Addendum, June 7, 2010: More goofs corrected. Misspellings this time.