Treating Hypothermia With Wet Blankets

Paul Krugman

What A Drag

From Goldman Sachs, an estimate of the federal budget impact on growth. The gray line shows the direct impact, the blue line includes the induced “multiplier” effects. Notice that this shows the rate of change, not the level effects. I explained the difference a while back.

What you can see is that the unwinding of the stimulus is a growing drag on growth. The GS economists warn that depending on how the budget battle plays out, things could be even worse.

The Street Light

Contractionary Fiscal Policiy and the US Job Market

The BLS released its estimates of employment and the unemployment rate for May. Unsurprisingly, it was a weak report, showing a marked slowdown in the US's net job creation in the private sector in May compared to preceding months.

The government sector of the economy continued to make the jobs picture worse. May was the seventh month in a row during which government layoffs undid some of the work of the private sector in creating jobs. Since January 2009, government employment has shrunk in 21 of 29 months -- and without temporary hiring for the Census, it would probably have shrunk in 25 of the last 29 months.

This steady reduction in government employment is a form of contractionary fiscal policy. (Note that most of the layoffs are at the state and local level, and thus are primarily composed of teachers and public safety personnel.) If government employment were simply keeping up with population growth in the US, we would expect to see about 17 to 18 thousand more state and local government jobs each month. Instead employment has shrunk by an average of 15 thousand jobs per month since the start of 2009.

The following chart shows what the monthly employment report would have looked like over the past 8 months (i.e. since the one-time effects of the Census that skewed employment from March-Sept of 2010) if government employment had simply kept up with the rate of population growth:

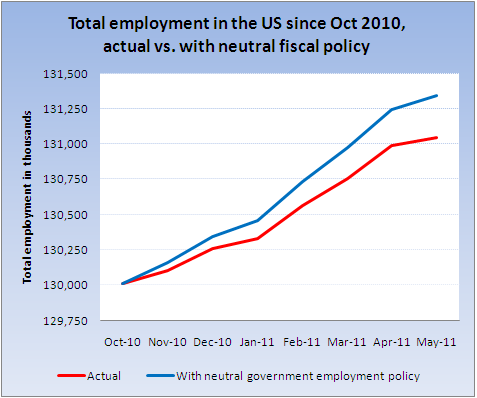

And total employment in the US would have followed the blue line in the chart below, rather than the red line:

In other words, in the absence of the sharp cutbacks in government spending that have been prevalent in the US over the past year or two, about 1.3 million additional people would be working now compared to 8 months ago, rather than the actual job growth we've experienced over that time of about 1 million - a 30% difference. That's a pretty tough headwind to fight, especially for an economy that's already struggling.

Federal Reserve Bank of New York

Commodity Prices and the Mistake of 1937: Would Modern Economists Make the Same Mistake?

(1) Signs indicate that the recession is finally over. (2) Short-term interest rates have been close to zero for years but are now expected to rise. (3) Some are concerned about excessive inflation. (4) Inflation concerns are partly driven by a large expansion in the monetary base in recent years and by banks’ massive holding of excess reserves. (5) Furthermore, some are worried that the recent rally in commodity prices threatens to ignite an inflation spiral.

While this summary arguably describes current trends, it is taken from an account of conditions in 1937 that appears in “The Mistake of 1937: A General Equilibrium Analysis,” an article I coauthored with Benjamin Pugsley. What we call “the Mistake of 1937” was, in broad terms, a decision by the Fed and the administration to implement a series of contractionary policies that choked off the recovery of 1933-37 and brought on the recession of 1937-38, one of the worst on record. What is particularly noteworthy is that the inflation fears that triggered the Mistake of 1937 were largely driven by a rally in commodity prices. These circumstances invite direct comparison with our own time, when a substantial recent rise in commodity prices (which now seems to be abating somewhat) stoked inflation fears and led some commentators to call for an increase in the federal funds rate...

The Mistake and Its Consequences

The Mistake of 1937 was a preemptive policy tightening in a fragile economic environment. Specifically, it was a decision to abandon the policy of “reflation” introduced in 1933. After prices tumbled during the 1929-33 depression, the administration of Franklin Delano Roosevelt (FDR) and the Federal Reserve made a commitment to increase the price level to pre-depression levels. (For more on this key initiative of the 1933-37 recovery period, see my article in the American Economic Review, “Great Expectations and the End of the Depression.”) The reflation policy was backed by an aggressive increase in government spending, the maintenance of large deficits, the abandonment of the gold standard, and monetary easing. If we accept the account of modern macroeconomic models, this reflationary policy mix can be very expansionary once the short-term interest rate is constrained at zero (as it was at the time). Why? Because at zero interest rates, if people start expecting that prices will rise instead of continuing to fall, the real rate of interest-a critical determinant of aggregate spending-turns from positive to negative. Thus, it becomes economical to spend money rather than save it. A further benefit of reflation is that it can repair balance sheets of overleveraged households and firms, a point explained in more detail in my recent paper with Paul Krugman, “Debt, Deleveraging, and the Liquidity Trap.”

The Mistake of 1937 was to relinquish the benefits of reflation and to set all policy levers in reverse. The Fed and key administration officials hinted at interest rate hikes and endorsed austerity in fiscal policy; the key concern now was containing inflation rather than sustaining recovery...