Swatting at the Swarm, Part III: Making an Asch of Us All

Unhappily for us all, we are surrounded by corporate accomplices willing to influence our hearts and minds. I gave you a taste of this in Part II. In at least three of the four examples I provided we find a strong fiduciary incentive to warrant the noted shenanigans, obvious reasons why the participants would go to such misinformation extremes. Toyota wanted to squelch as much of the criticism of its cars as it could. The Canadian recording industry stands to gain millions, perhaps billions, if it can in the future prevent even fair use infringements on its copyrights. Never mind the ideological victory it would prove; dismantling the social safety net might prove an enormous boon to private health care providers simply by impeding government efforts to reduce the current cost of health care ( which is, compared to the rest of the world, a tad expensive).

In Part I, I said early on that I wanted to focus primarily on how this swarm swatting, this manipulation of the crowd for fun and/or profit, deflects from our society's ability to make rational decisions regarding the economy. I'll stick to that aspect of society not to simply discount other, perhaps more pressing avenues of public controversy, but because the economy has, as bleaknemesis notes, a relatively weak moral component. Struck by Part I of this series, he said two weeks ago in an email:

I am thinking though that the ox situation and your own rent adjustment story may only work under certain conditions to validate the crowd wisdom and that under other conditions a less than wise outcome may occur. For this I am thinking of Nazi Germany or segregationist South US. Now I am aware that I might be trying to impose our current moral standards on the past which may not be fair. Actually as I was writing this and reading it over it occurred to me that maybe the reason the ox story works as an example for crowd wisdom is that there is no moral component to the weight guessing. Kind of the same with the rent story for the most part.

Mr. Nemesis, from all the reading I've done on this topic, you are absolutely correct on all points. Furthermore, you also mentioned a book I had either never heard of (or, more likely had forgotten about), James Surowiecki's The Wisdom of Crowds. I got the book from the library, and oh, boy, am I glad I did. Along with Steven Johnson's Emergence (which I've gushed about before), Wisdom proves one of the best synopses of crowd wisdom I've ever read. In fact, in the end notes Surowiecki mentions Emergence and notes how his direction with Wisdom differed from Johnson's:

There are obvious resonances between Johnson's book and my own, although in his model local influence is important and generally beneficial, while I see independence as essential and see influence as, on the whole, inimical to good cognitive judgments. On the other hand, local influence is clearly a good thing when it comes to coordination problems. More to the point, Emergence is only tangentially concerned with decision making, and is more interested in, as the title suggests, self-organization and the emergence of order.

(James Surowiecki, The Wisdom of Crowds, Doubleday, 2004, p. 282.)

We should discuss what Surowiecki means by "independence."

(T)he assumption of independence is a familiar one. It's intuitively appealing, since it takes the autonomy of the individual for granted. It's at the core of Western liberalism. And, in the form of what's usually called "methodological individualism," it underpins most of textbook economics. Economists usually take it as a given that people are self-interested. And they assume people arrive at their ideas of self-interest on their own.

For all this, though, independence is hard to come by. We are autonomous beings, but we are also social beings. We want to learn from each other, and learning is a social process. The neighborhoods where we live, the schools we attend, and the corporations where we work shape the way we think and feel. . . .

Even while recognizing . . . the social nature of existence, economists tend to emphasize people's autonomy and to downplay the influence of others on our preferences and judgments.

(Surowiecki, ibid, p. 42.)

Thus, there lies between the rugged "methodological individualism" of the economist an inherent contradiction, something noted by sociologists:

Sociologists and social-network theorists, by contrast, describe people as embedded in particular social contexts, and see influence as inescapable. Sociologists generally don't view this as a problem. They suggest it's simply the way human life is organized. And it may not be a problem for everyday life. But what I want to argue here is that the more influence a group's members exert on each other, and the more personal contact they have with each other, the less likely it is that the group's decision will be wise ones. The more influence we exert on each other, the more likely it is that we will believe the same things and make the same mistakes. That means it's possible that we could become individually smarter but collectively dumber.

(Surowiecki, ibid, emphasis mine.)

Ah, but Surowiecki has some very specific types of interactions in mind when he speaks of "influence." After all, a properly structured interaction invokes the very crowd wisdom he uses for his book's title. The wrong interactions . . . those are, as he noted in his comment on Emergence above, the ones to fear, the interactions creating influence that becomes "inimical to good cognitive judgments".

Surowiecki specifies that crowd independence preserves crowd wisdom in basically two different ways:

First, it keeps the mistakes that people make from becoming correlated. Errors in individual judgment won't wreck the group's collective judgment as long as those errors aren't systematically pointing in the same direction. One of the quickest ways to make people's judgments systematically biased is to make them dependent on each other for information. Second, independent individuals are more likely to have new information rather than the same old data everyone is already familiar with. The smartest groups, then, are made up of people with diverse perspectives who are able to stay independent of each other. Independence doesn't imply rationality or impartiality, though. You can be biased and irrational, but as long (as) you're independent, you won't make the group any dumber.

(Surowiecki, ibid, p. 41.)

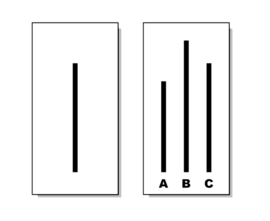

The first researcher we should discuss demonstrating exactly how both of these tightly-related variables could be compromised is psychology professor Solomon Asch. In the 1950s, Prof. Asch set out to determine how influential the stated opinions of others can be in swaying one's own opinion. According to Surowiecki and the Wiki entry covering the experiment:

the participants - the real subjects and the confederates - were all seated in a classroom. They were asked a variety of questions about the lines such as how long is A, compare the length of A to an everyday object, which line was longer than the other, which lines were the same length, etc. The group was told to announce their answers to each question out loud. The confederates always provided their answers before the study participant, and always gave the same answer as each other. They answered a few questions correctly but eventually began providing incorrect responses.

From this simple experiment, we may have first as a society noted how very susceptible we all are to the opinions of others, even opinions absent any moral component. Surowiecki describes what happened in the experiments:

The subject . . . sat there as everyone else in the room announced that the truth was something that he could plainly see was not true. Not surprisingly, this occasioned some bewilderment. The unwitting subjects changed the position of their heads to look at the lines from a different angle. They stood up to scrutinize the lines more closely. And they joked nervously about whether they were seeing things.

Most important, a significant number of the subjects simply went along with the group, saying that lines that were clearly shorter or longer than the line on the card were actually the same size. . . .

(Surowiecki, ibid, p. 38, emphasis mine.)

Just a few years before Asch's experiments, George Orwell in 1984 posited a dystopian future where a state government went to extreme lengths, including torture and brainwashing, to get its citizens to understand that 2+2=5. Asch shows, by contrast, that Orwell needn't have gone to such measures, since getting people to publicly declare what they know is not true is relatively simple. All you need are some accomplices.

Perhaps I've been too hard on our corporate media by accusing them of egregious manipulations designed to keep our attentions diverted from under-covered topics. Perhaps I should rather assume our corporate media is simply trying to do a good job, but just cocking things up a bit here and there for reasons other than overt malevolence and unseen affiliations.

Fine. I'll consider that angle, and throw in a bit of good news: Asch further discovered that, when the number of accomplices is reduced, so too is the conformity pressure on the subject.

Asch went on, though, to show something just as important: while people are willing to conform even against their own better judgment, it does not take much to get them to stop. In one variant on his experiment, for instance, Asch planted a confederate who, instead of going along with the group, picked the lines that matched the line on the card, effectively giving the unwitting subject an ally. And that was enough to make a huge difference. Having even one other person in the group who felt as they did made the subjects happy to announce their thoughts, and the rate of conformity plummeted.

(Surowiecki, ibid, p. 39.)

This means that any cabal pulling the media's puppet strings would have to have an enormous reach simply to squelch any dissenting voices, making a massive Orwellian vision a reality prohibitively difficult. Still, what happens when we consider (for one example) financial media merely incompetent? Shouldn't the public still get enough information to accurately judge the various markets well enough to participate profitably?

In The Ingenuity Gap, Thomas Homer-Dixon points out that the stock and bond markets suffer from "positive feedback:"

Feedback can be positive or negative. By "positive" feedback, complexity theorists don't mean that the feedback is always and "good" thing. Instead, they mean that the feedback reinforces or amplifies the initial change, and in the process it creates a virtuous or vicious circle. . . . (I)n a bull market, rising stock prices reinforce the confidence of investors, which causes them to buy more stocks, which further boosts prices; more begets more. This interaction is a virtuous circle, since most people become wealthier. In a bear market, falling prices undermine investors' confidence, which causes them to sell stocks and further drives down prices; less begets less -- a vicious circle, since most people become poorer. . . . The important thing about positive feedbacks is that they are inherently unstable: they create self-reinforcing spirals of behavior, and can cause systems to become overextended or unbalanced.

(Thomas Homer-Dixon, The Ingenuity Gap, Alfred A. Knopf, 2000, pp. 111-112, emphasizing again, I am.)

With this in mind, Surowiecki cites two studies that question how well news can affect the wisdom crowds in aggregate can create when that news is from a "trusted" source. The first employs a variant on Galton's ox weighing contest, the jelly bean experiment:

(Researcher Jack) Treynor had the students in his finance class guess the number of jelly beans in a jar. Nor surprisingly, the average guess was within 3 percent of the number of beans in the jar . . . and only one person in the class did better than the group as a whole. Up to this point, Treynor was demonstrating what Francis Galton's experiment with the ox had also shown.

Then Treynor had the students guess at the number of jelly beans again. This time, though, they were cautioned to think about the fact that there was air space at the top of the jar and that the jar was made of plastic, not glass, meaning that it could hold more beans than might have been expected. The group's average guess was off by 15 percent, and was considerably worse than the guesses of a number of the people in the class.

The point is that the information skewed the perspectives of the students in a shared way. What the students were told was true. But because it was a truth that seemed to point in one direction -- there were probably more beans in the jar than they believed -- it destroyed their collective wisdom. And the way the information was disclosed mattered. In a sense, instead of saying here are some jelly beans in a plastic jar, Treynor went out of his way to explain why he thought the plastic was important. In doing so, he subtracted information from the students. The more they were told, the less they actually knew about how many beans were in the jar.

(Surowiecki, ibid, p. 255, emphasis mine yet again.)

What Treynor discovered in a more controlled environment, Paul Andreassen discovered using almost exactly the same settings in which actual investors find themselves. Folks, this study truly surprised me. I cannot emphasize the importance of its findings enough.

Andreassen divided students into two groups. Each group selected a portfolio of stocks, and knew enough about each stock to come up with what seemed like a fair price for it. Then Andreassen allowed one group to see only the changes in the prices of their stocks. They could buy and sell if they wanted, but all they knew was whether the price of a stock had gone up or down. The second group was allowed to see the changes in price, but was also given a constant stream of financial news that supposedly explained what was happening. Surprisingly, the less-well-informed group did far better than the group that was given all the news.

(Surowiecki, ibid, p. 254, and really, how could I not emphasize?)

This result suggests that, when it comes to the information one needs to make good decisions, too much news can be a bad thing. "The reason, Andreassen suggested, was that news reports tend, by their nature, to overplay the importance of any particular piece of information," Surowiecki notes. Everyone in the jelly bean class could see that the beans were in a plastic jar and that they did not reach all the way to the top; Treynor's noting that, though, did for that information what the financial reporters do to just about any story, over-emphasize it and thus destroy the crowd's accuracy.

I got another nugget of gold from Surowiecki in his notes on the Andreassen experiment. He said, "This is really one of the more interesting papers in the experimental economics literature, yet it's rarely mentioned." (p. 295.) I agree; but I'm willing to speculate a guess as to why this is.

Consider, folks, the telly news common on our screens before Lewis Powell wrote his now-infamous memorandum a bit less than 40 years ago. Then, television stations and networks kept the news lean simply because it was what retailers call a "loss leader." Everyone by dint of their broadcasting licenses issued by the Federal Communications Commission had to provide news; that didn't make any of that news popular and thus a magnet for advertising dollars. All that started to change about thirty years ago as stations ramped up the hours dedicated to news coverage. News became a big draw, and was relatively inexpensive to produce.

This period of change had an effect on more than the number of news hours featured. How the news was shown changed dramatically, shifting from a dry behind-the-desk reportage of simple fact to a seeking of angle, a telling of a compelling story. News stories had to "grab" the viewers, no matter what the politicians and policy makers actually providing that news wanted. Sensationalism became more the norm. As Homer-Dixon notes, "Whereas journalists want their stories to have concreteness, plot line, color, real people, terseness, and above all 'an endless series of conflicts and momentary resolutions,' politicians want to preserve nuance and room to maneuver and compromise." (Homer-Dixon, ibid, pp. 321-322.)

Remember, all this happened -- and is happening -- in order to grab eyeballs and make them sticky enough on a particular screen to keep the viewer glued, to prevent him or her from flipping channels between commercials.

Financial news reporting proves no exception to this Golden Rule of commercial television. I'm quite sure someone at CNBC has read Andreassen's paper. It was published just about seven years after the network's founding, plenty of time to absorb his unique insight. After all, if what he demonstrates is true -- that their entire presentation of financial news is making their viewers stupider and individually more likely to lose money -- someone must think this is a problem.

But why would they?

Their business model has less to do with actually delivering content that could prove useful than in providing content, once again, that sells advertisements. The dry, fact-based, and unemotional narrative drone from the 60s is too far gone in the style book to ever make a comeback . . . even though it works better at informing people. If CNBC thinks hyperbole keeps people glued to the set, then hyperbole will rule the financial news day.

And they must be doing something right, even if it's not informing those viewers. "Seven million people a week watched CNBC at the market's peak," notes Surowiecki, "and if you were at all interested in the stock market, it was inescapable." (p. 252.)

That's a lot of advertising dollars.

So, from Asch we get a mechanism for changing minds (with just a little conspiratorial skull-duggery required), and from Treynor and Andreassen we see that just a little honest reporting, when done wrong, will actually lead the crowd in the wrong direction. Combine those basic studies, throw in a bit of vested interest, and it's easy to see how our current system of informing the populace may have created the havoc in which we currently find ourselves embroiled.

Ah, but it gets worse. I mentioned Thomas Homer-Dixon's book for a reason. With my background in Johnson's Emergence already in place, The Ingenuity Gap started my interest in this topic just a couple of months ago. Yes, we might be able to see how the people on the soapboxes are, either intentionally or not, leading the lemmings to the edge of the cliff; but even if those problems are addressed, would we be able to see the break in the landscape in time to avert disaster? And if we did, would we even know which way to turn? That's a topic to explore later.

In Part I, I said early on that I wanted to focus primarily on how this swarm swatting, this manipulation of the crowd for fun and/or profit, deflects from our society's ability to make rational decisions regarding the economy. I'll stick to that aspect of society not to simply discount other, perhaps more pressing avenues of public controversy, but because the economy has, as bleaknemesis notes, a relatively weak moral component. Struck by Part I of this series, he said two weeks ago in an email:

I am thinking though that the ox situation and your own rent adjustment story may only work under certain conditions to validate the crowd wisdom and that under other conditions a less than wise outcome may occur. For this I am thinking of Nazi Germany or segregationist South US. Now I am aware that I might be trying to impose our current moral standards on the past which may not be fair. Actually as I was writing this and reading it over it occurred to me that maybe the reason the ox story works as an example for crowd wisdom is that there is no moral component to the weight guessing. Kind of the same with the rent story for the most part.

Mr. Nemesis, from all the reading I've done on this topic, you are absolutely correct on all points. Furthermore, you also mentioned a book I had either never heard of (or, more likely had forgotten about), James Surowiecki's The Wisdom of Crowds. I got the book from the library, and oh, boy, am I glad I did. Along with Steven Johnson's Emergence (which I've gushed about before), Wisdom proves one of the best synopses of crowd wisdom I've ever read. In fact, in the end notes Surowiecki mentions Emergence and notes how his direction with Wisdom differed from Johnson's:

There are obvious resonances between Johnson's book and my own, although in his model local influence is important and generally beneficial, while I see independence as essential and see influence as, on the whole, inimical to good cognitive judgments. On the other hand, local influence is clearly a good thing when it comes to coordination problems. More to the point, Emergence is only tangentially concerned with decision making, and is more interested in, as the title suggests, self-organization and the emergence of order.

(James Surowiecki, The Wisdom of Crowds, Doubleday, 2004, p. 282.)

We should discuss what Surowiecki means by "independence."

(T)he assumption of independence is a familiar one. It's intuitively appealing, since it takes the autonomy of the individual for granted. It's at the core of Western liberalism. And, in the form of what's usually called "methodological individualism," it underpins most of textbook economics. Economists usually take it as a given that people are self-interested. And they assume people arrive at their ideas of self-interest on their own.

For all this, though, independence is hard to come by. We are autonomous beings, but we are also social beings. We want to learn from each other, and learning is a social process. The neighborhoods where we live, the schools we attend, and the corporations where we work shape the way we think and feel. . . .

Even while recognizing . . . the social nature of existence, economists tend to emphasize people's autonomy and to downplay the influence of others on our preferences and judgments.

(Surowiecki, ibid, p. 42.)

Thus, there lies between the rugged "methodological individualism" of the economist an inherent contradiction, something noted by sociologists:

Sociologists and social-network theorists, by contrast, describe people as embedded in particular social contexts, and see influence as inescapable. Sociologists generally don't view this as a problem. They suggest it's simply the way human life is organized. And it may not be a problem for everyday life. But what I want to argue here is that the more influence a group's members exert on each other, and the more personal contact they have with each other, the less likely it is that the group's decision will be wise ones. The more influence we exert on each other, the more likely it is that we will believe the same things and make the same mistakes. That means it's possible that we could become individually smarter but collectively dumber.

(Surowiecki, ibid, emphasis mine.)

Ah, but Surowiecki has some very specific types of interactions in mind when he speaks of "influence." After all, a properly structured interaction invokes the very crowd wisdom he uses for his book's title. The wrong interactions . . . those are, as he noted in his comment on Emergence above, the ones to fear, the interactions creating influence that becomes "inimical to good cognitive judgments".

Surowiecki specifies that crowd independence preserves crowd wisdom in basically two different ways:

First, it keeps the mistakes that people make from becoming correlated. Errors in individual judgment won't wreck the group's collective judgment as long as those errors aren't systematically pointing in the same direction. One of the quickest ways to make people's judgments systematically biased is to make them dependent on each other for information. Second, independent individuals are more likely to have new information rather than the same old data everyone is already familiar with. The smartest groups, then, are made up of people with diverse perspectives who are able to stay independent of each other. Independence doesn't imply rationality or impartiality, though. You can be biased and irrational, but as long (as) you're independent, you won't make the group any dumber.

(Surowiecki, ibid, p. 41.)

The first researcher we should discuss demonstrating exactly how both of these tightly-related variables could be compromised is psychology professor Solomon Asch. In the 1950s, Prof. Asch set out to determine how influential the stated opinions of others can be in swaying one's own opinion. According to Surowiecki and the Wiki entry covering the experiment:

the participants - the real subjects and the confederates - were all seated in a classroom. They were asked a variety of questions about the lines such as how long is A, compare the length of A to an everyday object, which line was longer than the other, which lines were the same length, etc. The group was told to announce their answers to each question out loud. The confederates always provided their answers before the study participant, and always gave the same answer as each other. They answered a few questions correctly but eventually began providing incorrect responses.

From this simple experiment, we may have first as a society noted how very susceptible we all are to the opinions of others, even opinions absent any moral component. Surowiecki describes what happened in the experiments:

The subject . . . sat there as everyone else in the room announced that the truth was something that he could plainly see was not true. Not surprisingly, this occasioned some bewilderment. The unwitting subjects changed the position of their heads to look at the lines from a different angle. They stood up to scrutinize the lines more closely. And they joked nervously about whether they were seeing things.

Most important, a significant number of the subjects simply went along with the group, saying that lines that were clearly shorter or longer than the line on the card were actually the same size. . . .

(Surowiecki, ibid, p. 38, emphasis mine.)

Just a few years before Asch's experiments, George Orwell in 1984 posited a dystopian future where a state government went to extreme lengths, including torture and brainwashing, to get its citizens to understand that 2+2=5. Asch shows, by contrast, that Orwell needn't have gone to such measures, since getting people to publicly declare what they know is not true is relatively simple. All you need are some accomplices.

Perhaps I've been too hard on our corporate media by accusing them of egregious manipulations designed to keep our attentions diverted from under-covered topics. Perhaps I should rather assume our corporate media is simply trying to do a good job, but just cocking things up a bit here and there for reasons other than overt malevolence and unseen affiliations.

Fine. I'll consider that angle, and throw in a bit of good news: Asch further discovered that, when the number of accomplices is reduced, so too is the conformity pressure on the subject.

Asch went on, though, to show something just as important: while people are willing to conform even against their own better judgment, it does not take much to get them to stop. In one variant on his experiment, for instance, Asch planted a confederate who, instead of going along with the group, picked the lines that matched the line on the card, effectively giving the unwitting subject an ally. And that was enough to make a huge difference. Having even one other person in the group who felt as they did made the subjects happy to announce their thoughts, and the rate of conformity plummeted.

(Surowiecki, ibid, p. 39.)

This means that any cabal pulling the media's puppet strings would have to have an enormous reach simply to squelch any dissenting voices, making a massive Orwellian vision a reality prohibitively difficult. Still, what happens when we consider (for one example) financial media merely incompetent? Shouldn't the public still get enough information to accurately judge the various markets well enough to participate profitably?

In The Ingenuity Gap, Thomas Homer-Dixon points out that the stock and bond markets suffer from "positive feedback:"

Feedback can be positive or negative. By "positive" feedback, complexity theorists don't mean that the feedback is always and "good" thing. Instead, they mean that the feedback reinforces or amplifies the initial change, and in the process it creates a virtuous or vicious circle. . . . (I)n a bull market, rising stock prices reinforce the confidence of investors, which causes them to buy more stocks, which further boosts prices; more begets more. This interaction is a virtuous circle, since most people become wealthier. In a bear market, falling prices undermine investors' confidence, which causes them to sell stocks and further drives down prices; less begets less -- a vicious circle, since most people become poorer. . . . The important thing about positive feedbacks is that they are inherently unstable: they create self-reinforcing spirals of behavior, and can cause systems to become overextended or unbalanced.

(Thomas Homer-Dixon, The Ingenuity Gap, Alfred A. Knopf, 2000, pp. 111-112, emphasizing again, I am.)

With this in mind, Surowiecki cites two studies that question how well news can affect the wisdom crowds in aggregate can create when that news is from a "trusted" source. The first employs a variant on Galton's ox weighing contest, the jelly bean experiment:

(Researcher Jack) Treynor had the students in his finance class guess the number of jelly beans in a jar. Nor surprisingly, the average guess was within 3 percent of the number of beans in the jar . . . and only one person in the class did better than the group as a whole. Up to this point, Treynor was demonstrating what Francis Galton's experiment with the ox had also shown.

Then Treynor had the students guess at the number of jelly beans again. This time, though, they were cautioned to think about the fact that there was air space at the top of the jar and that the jar was made of plastic, not glass, meaning that it could hold more beans than might have been expected. The group's average guess was off by 15 percent, and was considerably worse than the guesses of a number of the people in the class.

The point is that the information skewed the perspectives of the students in a shared way. What the students were told was true. But because it was a truth that seemed to point in one direction -- there were probably more beans in the jar than they believed -- it destroyed their collective wisdom. And the way the information was disclosed mattered. In a sense, instead of saying here are some jelly beans in a plastic jar, Treynor went out of his way to explain why he thought the plastic was important. In doing so, he subtracted information from the students. The more they were told, the less they actually knew about how many beans were in the jar.

(Surowiecki, ibid, p. 255, emphasis mine yet again.)

What Treynor discovered in a more controlled environment, Paul Andreassen discovered using almost exactly the same settings in which actual investors find themselves. Folks, this study truly surprised me. I cannot emphasize the importance of its findings enough.

Andreassen divided students into two groups. Each group selected a portfolio of stocks, and knew enough about each stock to come up with what seemed like a fair price for it. Then Andreassen allowed one group to see only the changes in the prices of their stocks. They could buy and sell if they wanted, but all they knew was whether the price of a stock had gone up or down. The second group was allowed to see the changes in price, but was also given a constant stream of financial news that supposedly explained what was happening. Surprisingly, the less-well-informed group did far better than the group that was given all the news.

(Surowiecki, ibid, p. 254, and really, how could I not emphasize?)

This result suggests that, when it comes to the information one needs to make good decisions, too much news can be a bad thing. "The reason, Andreassen suggested, was that news reports tend, by their nature, to overplay the importance of any particular piece of information," Surowiecki notes. Everyone in the jelly bean class could see that the beans were in a plastic jar and that they did not reach all the way to the top; Treynor's noting that, though, did for that information what the financial reporters do to just about any story, over-emphasize it and thus destroy the crowd's accuracy.

I got another nugget of gold from Surowiecki in his notes on the Andreassen experiment. He said, "This is really one of the more interesting papers in the experimental economics literature, yet it's rarely mentioned." (p. 295.) I agree; but I'm willing to speculate a guess as to why this is.

Consider, folks, the telly news common on our screens before Lewis Powell wrote his now-infamous memorandum a bit less than 40 years ago. Then, television stations and networks kept the news lean simply because it was what retailers call a "loss leader." Everyone by dint of their broadcasting licenses issued by the Federal Communications Commission had to provide news; that didn't make any of that news popular and thus a magnet for advertising dollars. All that started to change about thirty years ago as stations ramped up the hours dedicated to news coverage. News became a big draw, and was relatively inexpensive to produce.

This period of change had an effect on more than the number of news hours featured. How the news was shown changed dramatically, shifting from a dry behind-the-desk reportage of simple fact to a seeking of angle, a telling of a compelling story. News stories had to "grab" the viewers, no matter what the politicians and policy makers actually providing that news wanted. Sensationalism became more the norm. As Homer-Dixon notes, "Whereas journalists want their stories to have concreteness, plot line, color, real people, terseness, and above all 'an endless series of conflicts and momentary resolutions,' politicians want to preserve nuance and room to maneuver and compromise." (Homer-Dixon, ibid, pp. 321-322.)

Remember, all this happened -- and is happening -- in order to grab eyeballs and make them sticky enough on a particular screen to keep the viewer glued, to prevent him or her from flipping channels between commercials.

Financial news reporting proves no exception to this Golden Rule of commercial television. I'm quite sure someone at CNBC has read Andreassen's paper. It was published just about seven years after the network's founding, plenty of time to absorb his unique insight. After all, if what he demonstrates is true -- that their entire presentation of financial news is making their viewers stupider and individually more likely to lose money -- someone must think this is a problem.

But why would they?

Their business model has less to do with actually delivering content that could prove useful than in providing content, once again, that sells advertisements. The dry, fact-based, and unemotional narrative drone from the 60s is too far gone in the style book to ever make a comeback . . . even though it works better at informing people. If CNBC thinks hyperbole keeps people glued to the set, then hyperbole will rule the financial news day.

And they must be doing something right, even if it's not informing those viewers. "Seven million people a week watched CNBC at the market's peak," notes Surowiecki, "and if you were at all interested in the stock market, it was inescapable." (p. 252.)

That's a lot of advertising dollars.

So, from Asch we get a mechanism for changing minds (with just a little conspiratorial skull-duggery required), and from Treynor and Andreassen we see that just a little honest reporting, when done wrong, will actually lead the crowd in the wrong direction. Combine those basic studies, throw in a bit of vested interest, and it's easy to see how our current system of informing the populace may have created the havoc in which we currently find ourselves embroiled.

Ah, but it gets worse. I mentioned Thomas Homer-Dixon's book for a reason. With my background in Johnson's Emergence already in place, The Ingenuity Gap started my interest in this topic just a couple of months ago. Yes, we might be able to see how the people on the soapboxes are, either intentionally or not, leading the lemmings to the edge of the cliff; but even if those problems are addressed, would we be able to see the break in the landscape in time to avert disaster? And if we did, would we even know which way to turn? That's a topic to explore later.