Economics links

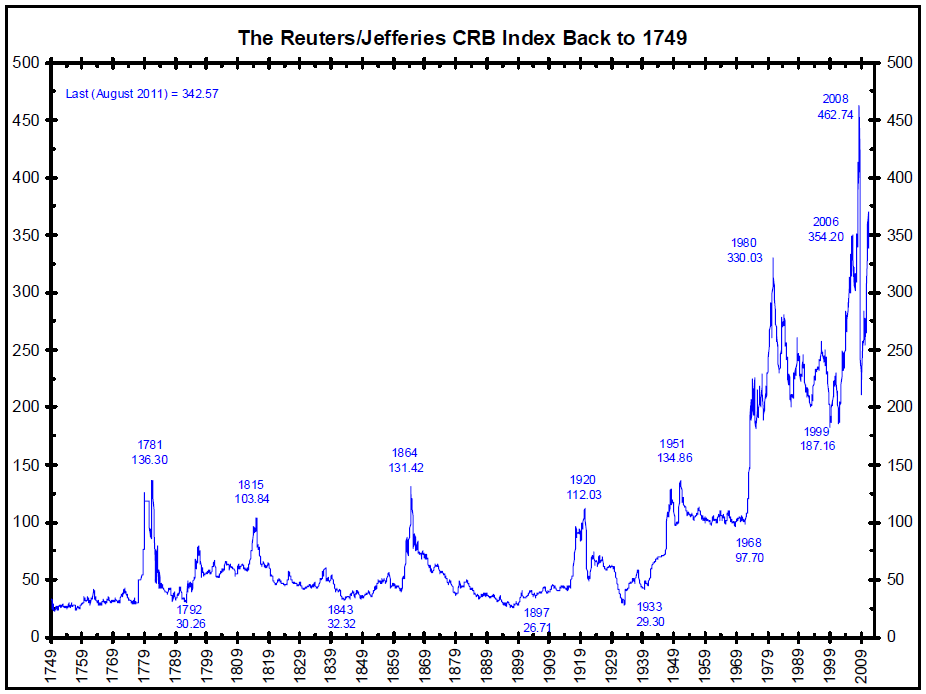

Commodity price index back to 1749.

Graphs allowing the comparing the fall in US spending on goods and services in 1929-33 to that during the “Great Recession”. Showing that the fall in US spending on goods and services during the Great Recession was by far the largest since 1960.

Arguing that the Copernican analogy actually shows how economics is more like other sciences.

Acknowledging an economic historian who acknowledged the failure of socialism (and then, as has been common, moved to environmentalism)

Looking at the problems of “peak oil”.

I support the “market monetarism” analysis of macroeconomics: their arguments and analysis is nicely summarised in this paper (pdf). A post with useful reading suggestions. My favourite economist has a post with links to his key posts and papers. Arguing that monetary policy should target spending as measured by nominal (money) GDP:

Between 2008 and 2009, NGDP declined at the fastest rate since 1938, while inflation (at least the "core" inflation rate, which excludes food and gas prices and which the Fed uses as its key inflation measure) raised no red flags. Because inflation cannot quickly adjust to such sudden drops in spending, this decline in nominal GDP brought about a sharp decline in real GDP - thus, a severe recession.

In an important sense, the sharp drop in NGDP precipitated the crisis: It was the proximate cause, even if the housing crisis was the ultimate cause. This suggests that NGDP is useful not only as a predictor and indicator of trouble, but as a target for monetary policy. Setting a goal in terms of nominal GDP could provide a superior alternative to the Fed's current inflation targets. …

As we shall see, inflation targeting can work, but only in a world in which policies explicitly aimed at raising the inflation rate are non-controversial. Obviously, we don't live in that world; in the universe we occupy, a nominal GDP target would be more effective.

Putting evidence that France might have been more to blame than (pdf) the US for the 1929-32 Depression:

France increased its share of world gold reserves from 7 percent to 27 percent between 1927 and 1932 and effectively sterilized most of this accumulation. This “gold hoarding” created an artificial shortage of reserves and put other countries under enormous deflationary pressure. Counterfactual simulations indicate that world prices would have increased slightly between 1929 and 1933, instead of declining calamitously, if the historical relationship between world gold reserves and world prices had continued. The results indicate that France was somewhat more to blame than the United States for the worldwide deflation of 1929-33. The deflation could have been avoided if central banks had simply maintained their 1928 cover ratios. …

countries not on the gold standard managed to avoid the Great Depression almost entirely, while countries on the gold standard did not begin to recover until after they left it. …

In December 1932, world gold reserves were 24 percent larger than they had been in December 1927. However, France absorbed almost every ounce of the additional gold, leaving the rest of the world with no net increase. …

For some reason, the world’s monetary gold stock was not being translated into world prices. The likely reason for this was the effective reduction in the monetized gold stock due to the sterilization of gold inflows by France and the United States. …

From this simple exercise, we can conclude that the Federal Reserve and Bank of France account for nearly all of the 30 percent worldwide deflation experienced in 1930 and 1931. …

In the United States, George Warren and Frank Pearson (1933, 125) were pushing a similar line about the problems with the gold standard: “The present depression is not an act of God for the purification of men’s souls. It is not a business cycle. It is not due to extravagant living. It is not due to unsound business practices. It is not due to too great efficiency. It is not due to lack of confidence, but is the cause of lack of confidence. It is due to high demand for gold following a period of low demand for gold. It teaches the devastating effects of deflation, but teaches no other lesson that is good for society.”

Placing current debates over the 1930s in the US within a single graph. The 1937-8 recession (one of the three worst US downturns in the C20th, the others being 1920-1 and 1929-30) as caused by a severe monetary shock:

The recession of 1937-38 occurred long ago, but it does have policy lessons for today. It suggests that, in a weak recovery, a pre-emptive monetary strike against inflation (which was very low at the time, as it is today) is capable of producing a devastating recession.

About trying to make central banks accountable for passive tightening of monetary policy.

An allegedly pro-market economist providing an analysis that massively discounts market information.

Putting the case for further “quantitative easing” (pdf) and arguing that, if Milton Friedman was still alive, he would be leading the charge for it. Finding the case persuasive.

The Swiss National Bank shows itself willing to do what it takes.

Amusingly arguing that the eurozone should get rid of Germany. (The point of the euro was a “deutschmark for everyone”, but the post does point to some real difficulties.) Krugman on the European Central Banks’s “catastrophic stability”.

Consumption and investment in the US both remain well below trend. IT has come to dominate US investment.

The sluggish recovery from the “Great Recession” in the US conforms to banking crises patterns. Changes in employment patterns in the US since the late 1970s. The disconnect between pay and productivity since 1980.

Pointing out how un-reassuring reports of President Obama’s economic views are. Noting the reported comment is compatible with his public comments.

The US Federal Income tax has become steadily more progressive (pdf) over the last 15 years.

Wayne Swan awarded finance minister of the year: getting the kudos for Glenn Stevens’ good work.

{kind=link}

Graphs allowing the comparing the fall in US spending on goods and services in 1929-33 to that during the “Great Recession”. Showing that the fall in US spending on goods and services during the Great Recession was by far the largest since 1960.

{kind=link}

{kind=link}

Arguing that the Copernican analogy actually shows how economics is more like other sciences.

Acknowledging an economic historian who acknowledged the failure of socialism (and then, as has been common, moved to environmentalism)

Looking at the problems of “peak oil”.

I support the “market monetarism” analysis of macroeconomics: their arguments and analysis is nicely summarised in this paper (pdf). A post with useful reading suggestions. My favourite economist has a post with links to his key posts and papers. Arguing that monetary policy should target spending as measured by nominal (money) GDP:

Between 2008 and 2009, NGDP declined at the fastest rate since 1938, while inflation (at least the "core" inflation rate, which excludes food and gas prices and which the Fed uses as its key inflation measure) raised no red flags. Because inflation cannot quickly adjust to such sudden drops in spending, this decline in nominal GDP brought about a sharp decline in real GDP - thus, a severe recession.

In an important sense, the sharp drop in NGDP precipitated the crisis: It was the proximate cause, even if the housing crisis was the ultimate cause. This suggests that NGDP is useful not only as a predictor and indicator of trouble, but as a target for monetary policy. Setting a goal in terms of nominal GDP could provide a superior alternative to the Fed's current inflation targets. …

As we shall see, inflation targeting can work, but only in a world in which policies explicitly aimed at raising the inflation rate are non-controversial. Obviously, we don't live in that world; in the universe we occupy, a nominal GDP target would be more effective.

Putting evidence that France might have been more to blame than (pdf) the US for the 1929-32 Depression:

France increased its share of world gold reserves from 7 percent to 27 percent between 1927 and 1932 and effectively sterilized most of this accumulation. This “gold hoarding” created an artificial shortage of reserves and put other countries under enormous deflationary pressure. Counterfactual simulations indicate that world prices would have increased slightly between 1929 and 1933, instead of declining calamitously, if the historical relationship between world gold reserves and world prices had continued. The results indicate that France was somewhat more to blame than the United States for the worldwide deflation of 1929-33. The deflation could have been avoided if central banks had simply maintained their 1928 cover ratios. …

countries not on the gold standard managed to avoid the Great Depression almost entirely, while countries on the gold standard did not begin to recover until after they left it. …

In December 1932, world gold reserves were 24 percent larger than they had been in December 1927. However, France absorbed almost every ounce of the additional gold, leaving the rest of the world with no net increase. …

For some reason, the world’s monetary gold stock was not being translated into world prices. The likely reason for this was the effective reduction in the monetized gold stock due to the sterilization of gold inflows by France and the United States. …

From this simple exercise, we can conclude that the Federal Reserve and Bank of France account for nearly all of the 30 percent worldwide deflation experienced in 1930 and 1931. …

In the United States, George Warren and Frank Pearson (1933, 125) were pushing a similar line about the problems with the gold standard: “The present depression is not an act of God for the purification of men’s souls. It is not a business cycle. It is not due to extravagant living. It is not due to unsound business practices. It is not due to too great efficiency. It is not due to lack of confidence, but is the cause of lack of confidence. It is due to high demand for gold following a period of low demand for gold. It teaches the devastating effects of deflation, but teaches no other lesson that is good for society.”

Placing current debates over the 1930s in the US within a single graph. The 1937-8 recession (one of the three worst US downturns in the C20th, the others being 1920-1 and 1929-30) as caused by a severe monetary shock:

The recession of 1937-38 occurred long ago, but it does have policy lessons for today. It suggests that, in a weak recovery, a pre-emptive monetary strike against inflation (which was very low at the time, as it is today) is capable of producing a devastating recession.

About trying to make central banks accountable for passive tightening of monetary policy.

An allegedly pro-market economist providing an analysis that massively discounts market information.

Putting the case for further “quantitative easing” (pdf) and arguing that, if Milton Friedman was still alive, he would be leading the charge for it. Finding the case persuasive.

The Swiss National Bank shows itself willing to do what it takes.

Amusingly arguing that the eurozone should get rid of Germany. (The point of the euro was a “deutschmark for everyone”, but the post does point to some real difficulties.) Krugman on the European Central Banks’s “catastrophic stability”.

Consumption and investment in the US both remain well below trend. IT has come to dominate US investment.

The sluggish recovery from the “Great Recession” in the US conforms to banking crises patterns. Changes in employment patterns in the US since the late 1970s. The disconnect between pay and productivity since 1980.

Pointing out how un-reassuring reports of President Obama’s economic views are. Noting the reported comment is compatible with his public comments.

The US Federal Income tax has become steadily more progressive (pdf) over the last 15 years.

Wayne Swan awarded finance minister of the year: getting the kudos for Glenn Stevens’ good work.